Dollar continues to power up today, as traders are rethinking Fed’s policy path ahead. The odds of a hold at June 14 FOMC meeting has dropped to around 60%, as the economy continued to show resilience. The strong stock market rally this week is also helping. Canadian Dollar is currently following as second best, and then Swiss Franc. Aussie is the worst performer for the day so far, followed by Euro and Kiwi. While Yen is still the biggest loser for the week, selling has somewhat slowed a bit.

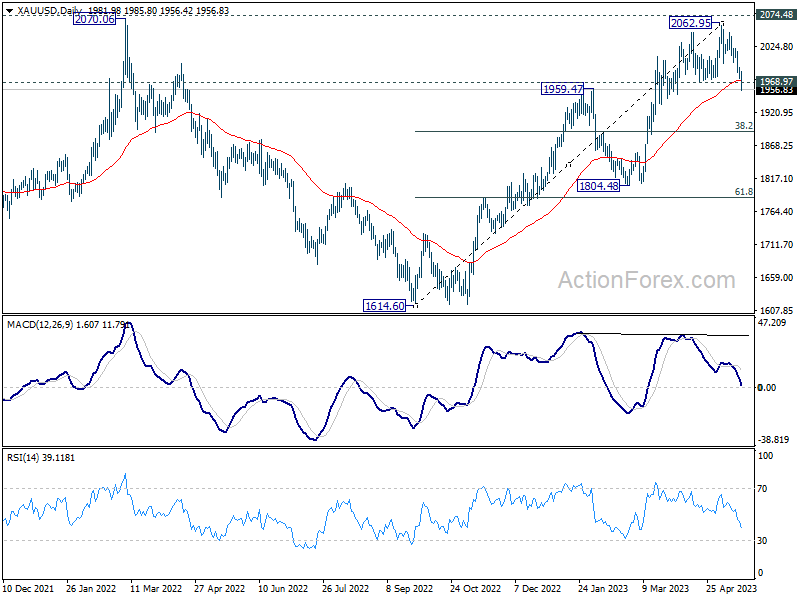

Technically, Gold has finally taken out 1968.97 key near term support, as well as 55 D EMA today, as selloff from 2062.95 extends. The development should confirm rejection by 2074.48 record high. Fall from 2062.95 is at least a correction to rise from 1614.60, with potential as the fifth leg of the long term sideway pattern from 2074.48. In either case, deeper decline is now expected to 38.2% retracement of 1614.60 to 2062.95 at 1891.69.

In Europe, at the time of writing, FTSE is up 0.38%. DAX is up 1.17%. CAC is up 0.62%. Germany 10-year yield is up 0.0971 at 2.438. Earlier in Asia, Nikkei rose 1.60%. Hong Kong HSI rose 0.85%. China Shanghai SSE rose 0.40%. Singapore Strait Times rose 0.27%. Japan 10-year JGB yield rose 0.0156 to 0.385.

Fed Logan: We haven’t yet made the progress we need to make

Dallas Fed Lorie Logan said in speech, “after raising the target range for the federal funds rate at each of the last 10 FOMC meetings, we have made some progress.”

Logan noted, “The data in coming weeks could yet show that it is appropriate to skip a meeting. As of today, though, we aren’t there yet.”

Addressing the inflation target, Logan emphasized the challenges that remain. “We haven’t yet made the progress we need to make. And it’s a long way from here to 2% inflation,” she remarked.

US initial jobless claims dropped back to 242k, below expectation

US initial jobless claims dropped -22k to 242k in the week ending May 13, below expectation of 260k. Four-week moving average of initial claims dropped -1k to 244k.

Continuing claims dropped -8k to 1799k in the week ending May 6. Four-week moving average of continuing claims dropped -15.5k to 1812.5k.

BoE Bailey not seeing balance sheet returning to pre-financial crisis levels

In his remarks to the Treasury Committee, BoE Governor Bailey commented that he does not foresee the BoE’s balance sheet returning to pre-financial crisis levels. Instead, he envisages a more proactive adjustment strategy, stating, “The Bank wants to adjust its balance sheet so that it has headroom to do whatever it might need to do in the future. It does not want its balance sheet to simply get larger after every economic shock.”

In a rebuttal to critics linking the UK’s inflation surge to QE policies, Bailey downplayed the connection, suggesting that the impact of COVID-19 supply chain disruptions was likely time-limited. “If the only shock that the world had experienced was that one [the Covid-19 supply chain disruption] then I think the evidence now suggests it had a limited time period. Unfortunately, of course, Ukraine came along, and there was no gap between these shocks,” he explained.

Deputy governor Ben Broadbent supported Bailey’s perspective, noting that the UK, along with other regions such as the US and the Eurozone, had engaged in a decade of QE without witnessing an inflation problem or robust money growth.

Addressing concerns about housing prices, Bailey refuted suggestions that the BoE’s policies had contributed to a surge. “Actually, the period in which the house price to income ratio rose most was the period of 10 years before 2007. That was the period when it rose most substantially. It hasn’t done the same thing since then,” he noted.

Australia employment down -4.3k in Apr, unemployment rate up to 3.7%

Australia employment contracted -4.3k in April, much worse than expectation of 25k growth. Full time job decreased -27.1k while part-time jobs rose 22.8k. Unemployment rate rose from 3.5% to 3.7%, above expectation of being unchanged at 3.5%. Participation rate dropped -0.1% to 66.7%. Employment-to-population ratio fell -0.2% to 64.2%. Monthly hours worked rose 2.6% mom or 49m hours.

Bjorn Jarvis, ABS head of labour statistics, said: “The small fall in employment followed an average monthly increase of around 39,000 people during the first quarter of this year.” Meanwhile, both employment-to-population ratio and participation rate “were still well above pre-COVID-19 pandemic levels and close to their historical highs in 2022”.

Japan’s exports grow at slowest pace since Feb 2021 despite setting record high for Apr

Japan’s exports grew by a modest 2.6% yoy to JPY 8288B in April. Although this represented the lowest growth in exports since February 2021, it still marked the largest export figure for April on record.

A closer examination of the data reveals a shift in trading dynamics. Exports to China fell by -2.9% yoy, marking the fifth consecutive month of decline. The decrease was driven by downturns in shipments of cars, car parts, and steel. Similarly, exports to Asia overall declined by -6.6% yoy, continuing a contraction trend for the fourth month in a row.

However, things looked rosier elsewhere. Exports to the US and EU showed robust growth, rising by 10.5% yoy and 11.7% yoy respectively. This uptick was led by a rebound in exports of cars and car parts, which have seen easing supply constraints.

Contrasting with export trends, imports fell by -2.3% yoy to JPY 8721B, the first annual decline witnessed in 27 months. This decrease was largely attributed to a slump in imports of crude oil and liquefied natural gas. Consequently, Japan recorded a trade deficit of JPY -432B for the 21st month running.

In seasonally adjusted term, the situation presents a slightly different picture. Exports rose by 2.5% mom to JPY 8259B, while imports inched up by 0.1% mom to JPY 9276B. In light of this, trade deficit narrowed to JPY -1017B.

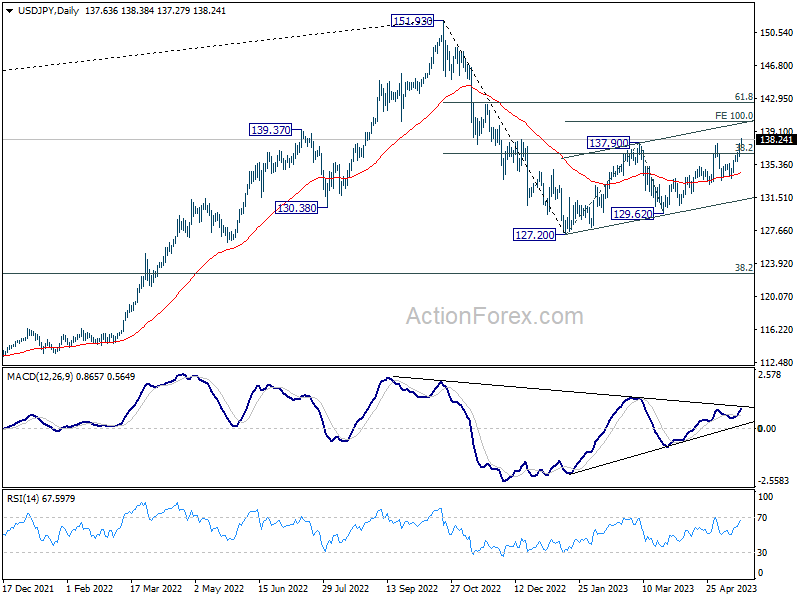

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 136.78; (P) 137.24; (R1) 138.18; More…

USD/JPY’s rally continues today and break of 137.90 resumes indicate resumption of whole rebound from 127.20. Intraday bias stays on the upside. Next target is 100% projection of 127.20 to 137.90 from 129.62 at 140.32. Break there will target 142.48 fibonacci level. On the downside, below 137.27 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 151.93 high are currently seen as a corrective pattern to the long term up trend. The first leg should have completed at 127.20. Rebound from there is seen as the second leg. Sustained break of 38.2% retracement of 151.93 to 127.20 at 136.34 will bring stronger rise to 61.8% retracement at 142.48. Meanwhile, break of 129.62 will argue that the third leg is starting through 127.20 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | PPI Input Q/Q Q1 | 0.20% | 0.50% | 0.50% | |

| 22:45 | NZD | PPI Output Q/Q Q1 | 0.30% | 0.80% | 0.90% | |

| 23:50 | JPY | Trade Balance (JPY) Apr | -1.02T | -1.08T | -1.21T | |

| 01:30 | AUD | Employment Change Apr | -4.3K | 25K | 53K | 61.1K |

| 01:30 | AUD | Unemployment Rate Apr | 3.70% | 3.50% | 3.50% | |

| 12:30 | CAD | New Housing Price Index M/M Apr | -0.10% | -0.10% | 0.00% | |

| 12:30 | USD | Initial Jobless Claims (May 12) | 242K | 260K | 264K | |

| 12:30 | USD | Philadelphia Fed Survey May | -10.4 | -20 | -31.3 | |

| 14:00 | USD | Existing Home Sales Apr | 4.35M | 4.44M | ||

| 14:30 | USD | Natural Gas Storage | 109B | 78B |