Dollar selloff resumes today on the back of extended rally in the stock markets and decline in treasury yields. Selloff in particularly apparent against Euro and Sterling, and to a slightly lesser extent Aussie. Yen also manages to resumes recent rally against the greenback. But Swiss Franc is lagging behind, as dragged down by selloff against other Europeans.

Technically, Sterling appears to have an advantage over Euro, with EUR/GBP dipping today. Break of 0.8689 minor support will likely resume the fall from 0.9267 through 0.8570 low. Nevertheless, firstly, the cross will have too take out mentioned 0.8689 minor support first. Secondly, the Pound will also face some tests from economic data release, and more importantly, the government’s new budget later in the week.

In Europe, at the time of writing, FTSE is up 0.33%. DAX is up 0.88%. CAC is up 1.09%. Germany 10-year yield is down -0.062 at 2.084. Earlier in Asia, Nikkei rose 0.10%. Hong Kong HSI rose 4.11%. China Shanghai SSE rose 1.64%. Singapore Strait Times rose 0.44%. Japan 10-year JGB yield rose 0.0012 to 0.244.

US PPI at 0.2% mom, 8.0% yoy in Oct

US PPI for final demand rose 0.2% mom in October, below expectation of 0.5% mom. Prices for goods rose 0.6% mom while services dropped -0.1% mom. PPI less foods, energy and trade services rose 0.2% mom.

For the 12 months period, PPI slowed from 8.4% yoy to 8.0% yoy. PPI less foods, energy, and trade services rose 5.4% yoy.

Also released, Empire State manufacturing index rose sharply from -9.1 to 4.5 in November, above expectation of -7.

German ZEW rose sharply to -36.7, related to hope that inflation will fall soon

Germany ZEW Economic Sentiment rose from -59.2 to -36.7 in November, much better than expectation of -54.1. Current Situation index rose from -72.2 to -64.5, above expectation of -67.5.

Eurozone ZEW Economic Sentiment rose from -59.7 to -38.7, above expectation of -55.0. Current Situation index rose 5.5pts to -65.1.

“The ZEW Indicator of Economic Sentiment rises again in November. This is likely to be related above all to the hope that inflation rates will fall soon. In this case, policymakers would not have to hit the brakes on monetary policy as hard and/or for as long as feared. However, the economic outlook for the German economy is still clearly negative,” comments ZEW President Professor Achim Wambach.

Eurozone goods exports rose 23.6% yoy in Sep, imports rose 44.5% yoy

In September, Eurozone goods exports, to the rest of the world, grew 23.6% yoy to EUR 210.1B. Goods imports rose 44.5% yoy to EUR 294.0B. Goods trade deficit came in at EUR -34.4B. Intra-Eurozone trade rose 27.3% yoy to EUR 247.6B.

In seasonally adjusted terms, Eurozone exports rose 1.6% mom to EUR 250.0B. Imports dropped -2.0% mom to EUR 287.7B. Trade deficit narrowed from EUR -47.6B to EUR -37.7B. Intra-Eurozone trade dropped from EUR 241.8B to EUR 238.9B.

According to the second estimate, Eurozone GDP grew 0.2% qoq in Q3, slowed from Q2’s 0.8% qoq. Employment grew 0.2% qoq, slowed from Q2’s 0.4% qoq.

UK payrolled employees rose 74k in Oct, unemployment rate at 3.6% in Sep

In October, UK payrolled employees rose 0.2% mom or 74k. Comparing with October 2021, payrolled employees rose 2.7% yoy or 772k. Median monthly pay rose 6.0% yoy. Claimant counts rose 3.3k, versus expectation of -12.6k.

In the three months to September, comparing to the previous three month period, unemployment was down -0.2% to 3.6%. Employment rate was unchanged at 75.5%. Economic inactivity rate rose 0.2% to 21.6%. Average earnings excluding bonus rose 5.7% yoy. Average earnings including bonus rose 6.0% yoy.

RBA minutes: Not ruling out returning to larger hikes

Minutes of RBA’s November 1 meeting revealed that board members consider both a 25 bps or a 50bps rate hike. There were “arguments in favour of both courses of action”, but the case for 25bps was stronger.

“Acknowledging the uncertainty, members did not rule out returning to larger increases if the situation warranted,” the minutes noted. “Conversely, the Board is prepared to keep rates unchanged for a period while it assesses the state of the economy and the inflation outlook. Interest rates are not on a pre-set path.”

At the meeting, RBA raised the cash rate target by 25bps to 2.85%.

Japan GDP contracted -0.3% qoq in Q3

Japan GDP contracted -0.3% qoq in Q3, much worse than expectation of 0.3% qoq. In annualized term, GDP contracted -1.2%, versus expectation of 1.1%. GDP deflator dropped -0.5% yoy, versus expectation of -0.2% yoy.

During the quarter, imports rose strongly by 5.2% yoy on higher energy costs and weak Yen exchange rate. Exports grew only 1.9% qoq and led to a decline in net exports, which dragged GDP down. Domestically, private consumption grew 0.3% qoq only.

“Increased imports due to the easing of supply constraints and a temporary increase in payments for external services contributed to the negative growth,” Chief Cabinet Secretary Hirokazu Matsuno said.

“The environment surrounding households and businesses is becoming more difficult, with declining real household incomes and rising corporate costs,” Matsuno added.

China retail sales contracted -0.5% yoy in Oct

China industrial production rose 5.0% yoy in October, below expectation of 5.2% yoy. Retail sales dropped -0.5% yoy, much worse than expectation of 1.0% yoy. That’s also the first decline since May. Fixed asset investment rose 5.8% ytd yoy, below expectation of 5.9%.

“We will focus on expanding effective demand, deepening structural reform on the supply side, continuing to stabilise employment and prices, stabilizing expectations, stimulating market vitality more, consolidating the economic recovery to a sound basis, and try to achieve better development results,” the NBS said in a statement.

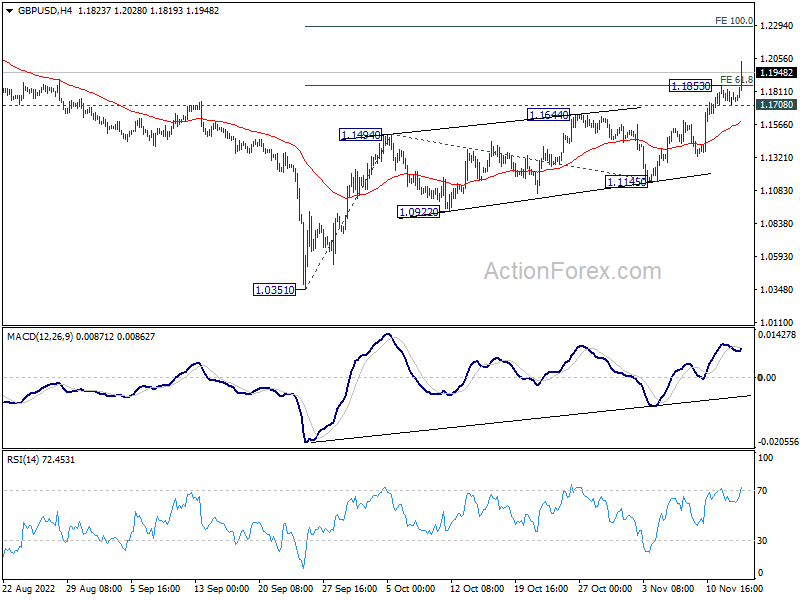

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1703; (P) 1.1766; (R1) 1.1821; More…

GBP/USD’s rise from 1.0351 resumed after brief retreat and intraday bias is back on the upside. With break of 61.8% projection of 1.0351 to 1.1494 from 1.1145 at 1.1851, next target will be 100% projection at 1.2288. On the downside, break of 1.1708 minor support will turn intraday bias neutral and bring consolidation again, before staging another rally.

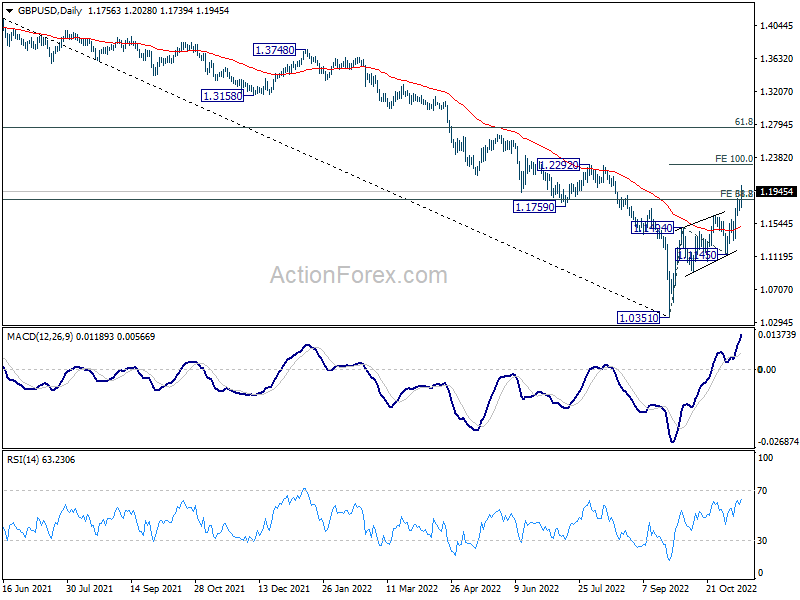

In the bigger picture, current development suggests that rise from 1.0351 is a medium term bottom. Rise from there is at least correcting whole down trend from 1.4248 (2021 high). Further rise is expected as long as 1.1145 support holds. Sustained break of 38.2% retracement of 1.4248 to 1.0351 at 1.1840 should pave the way to 61.8% retracement at 1.2759 and possibly above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Q/Q Q3 P | -0.30% | 0.30% | 0.90% | |

| 23:50 | JPY | GDP Deflator Y/Y Q3 P | -0.50% | -0.60% | -0.30% | |

| 00:30 | AUD | RBA Meeting Minutes | ||||

| 02:00 | CNY | Industrial Production Y/Y Oct | 5.00% | 5.20% | 6.30% | |

| 02:00 | CNY | Retail Sales Y/Y Oct | -0.50% | 1.00% | 2.50% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Oct | 5.80% | 5.90% | 5.90% | |

| 04:30 | JPY | Industrial Production M/M Sep F | -1.70% | -1.60% | -1.60% | |

| 07:00 | GBP | Claimant Count Change Oct | 3.3K | -12.6K | 25.5K | |

| 07:00 | GBP | Unemployment Rate (3M) Sep | 3.60% | 3.50% | 3.50% | |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Sep | 5.70% | 5.60% | 5.40% | |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Sep | 6.00% | 6.00% | 6.00% | |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Sep | -37.7B | -39.4B | -47.3B | -47.6B |

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | 0.20% | 0.20% | 0.20% | |

| 10:00 | EUR | Eurozone Employment Change Q/Q Q3 P | 0.20% | 0.30% | 0.40% | |

| 10:00 | EUR | Germany ZEW Economic Sentiment Nov | -36.7 | -54.1 | -59.2 | |

| 10:00 | EUR | Germany ZEW Current Situation Nov | -64.5 | -67.5 | -72.2 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Nov | -38.7 | -55 | -59.7 | |

| 13:30 | CAD | Manufacturing Sales M/M Sep | 0.00% | -0.50% | -2.00% | -1.90% |

| 13:30 | CAD | Wholesale Sales M/M Sep | 0.10% | -0.20% | 1.40% | 1.90% |

| 13:30 | USD | Empire State Manufacturing Index Nov | 4.5 | -7 | -9.1 | |

| 13:30 | USD | PPI M/M Oct | 0.20% | 0.50% | 0.40% | 0.20% |

| 13:30 | USD | PPI Y/Y Oct | 8% | 8.30% | 8.50% | 8.40% |

| 13:30 | USD | PPI Core M/M Oct | 0.00% | 0.40% | 0.30% | 0.20% |

| 13:30 | USD | PPI Core Y/Y Oct | 6.70% | 7.20% | 7.20% |