Dollar surges overnight after much hawkish than expected Fed interest rate projections. The case of near term bullish reversal continues to build up and there is prospect of further rally before weekend. Markets are relatively mixed elsewhere though. Australian Dollar is lifted by strong job data while New Zealand Dollar is supported by strong GDP. Yet, there is no follow through buying. Euro turned weaker but still, the selloff is not disastrous in crosses.

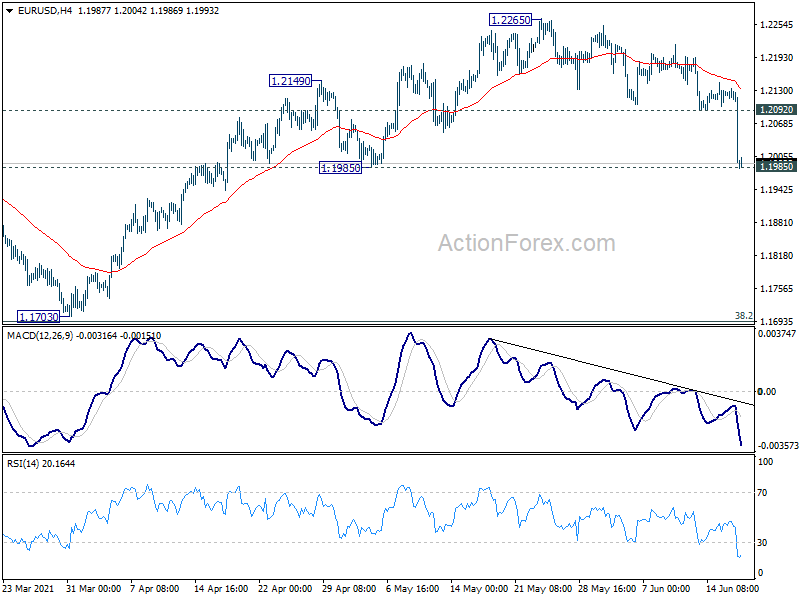

Technically, Dollar’s rally gather momentum with break of 1.4033 support in GBP/USD, 0.7644 support in AUD/USD, 0.9052 resistance in USD/CHF, 110.32 resistance in USD/JPY and 1.2201 resistance in USD/CAD. With 1.2 handle taken out, a major focus now is on 1.1985 support in EUR/USD. Sustained break of this level would likely drag EUR/USD towards 1.1703 medium term trend defining support.

In Asia, at the time of writing, Nikkei is down -1.15%. Hong Kong HSI is up 0.31%. China Shanghai SSE is up 0.17%. Singapore Strait Times is up 0.21%. Japan 10-year JGB yield is up 0.0156 at 0.065. Overnight, DOW dropped -0.77%. S&P 500 dropped -0.54%> NASDAQ dropped -0.24%. 10-year yield rose 0.070 to 1.569.

Fed stood pat but published hawkish projections

The Fed has turned more hawkish at the meeting overnight. Besides significant upgrades in the GDP growth and inflation forecasts, the median dot plots now project two rate hikes in 2023, compared with no rate hike until 2024. At the press conference, Fed chair Jerome Powell indicated that the members have started talking about tapering. He added that”while reaching substantial further progress is still a ways off, in coming meetings, the committee will assess progress”.

More on FOMC:

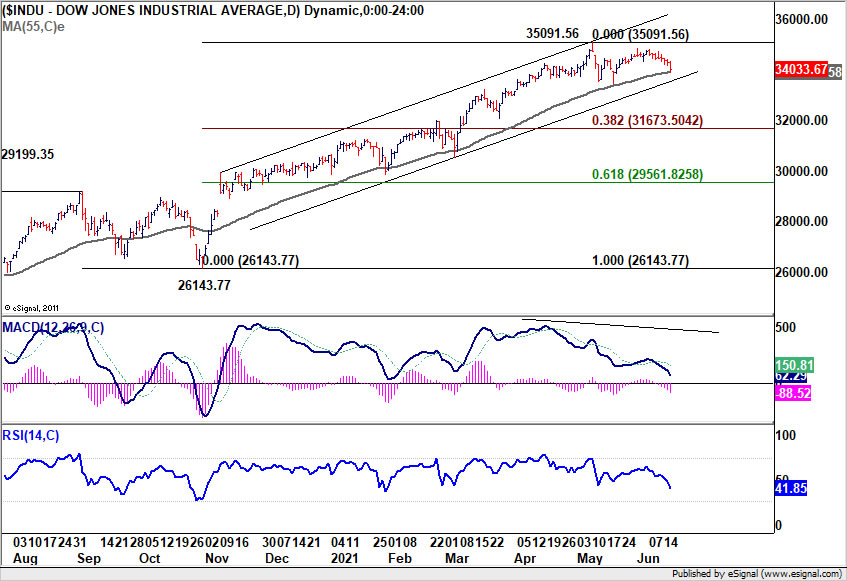

DOW dropped after hawkish Fed, but no threat to up trend yet

US stocks tumbled overnight after much more hawkish than expected FOMC projections. But the three major indices managed to pare back much of earlier losses to close just slightly lower. DOW lost -0.77%, S&P 500 dropped -0.54%, while NASDAQ declined -0.24%.

As for DOW, it’s still holding on to 55 day EMA, and stay well inside the medium term rising channel. Thus, there is no threat to the up trend for the moment. Another rise through 35091.56 is still in favor. But the next few days will be crucial on whether selloff could gather momentum. Firm break of the channel support would likely bring a correction to whole rise from 26143.77, and target 38.2% retracement at 31673.50.

10-year yield also jumped notably and closed up 0.070 to 1.569. Price actions from 1.765 high are clearly corrective and medium term up trend is expected to resume at a later stage. But the timing of an upside breakout would very much depend on development in stocks and upcoming economic data.

BoC Macklem: A complete recovery will still take some time

BoC Governor Tiff Macklem told a Senate Committee yesterday that “economy recovery is making good progress”. But “a complete recovery will still take some time”. He reiterated that BoC “remains steadfast in its commitment to support Canadian households and businesses through the full length of the recovery”.

A “complete recovery” means a “healthy job market”, while companies are “investing to seize new business opportunities. Also, households and businesses can “count on inflation being sustainably at our 2 percent target”.

Macklem also reiterated: ‘Looking ahead, further adjustments to the pace of net purchases will be guided by our ongoing assessment of the strength and durability of the economic recovery. If the recovery evolves in line with or stronger than our latest projection, the economy won’t need as much QE stimulus over time.”

Australia employment grew 115.2k in May, unemployment drop to pre-pandemic 5.1%

Australia employment rose 115.2k in May, above expectation of 30.0k. Full time jobs grew 97.5k. Part-time jobs rose 17.7k. Unemployment rate dropped to 5.1%, down from 5.5%, much better than expectation of of 5.5%. Participation rate also rose 0.3% to 66.2%.

Bjorn Jarvis, head of labour statistics at the ABS, said May was the seventh consecutive monthly fall in the unemployment rate. “The unemployment rate fell to 5.1 per cent, which was below March 2020 (5.3 per cent) and back to the level in February 2020 (5.1 per cent). The declining unemployment rate continues to align with the strong increases in job vacancies”.

New Zealand GDP grew 1.6% qoq in Q1, broad based growth

New Zealand GDP grew 1.6% qoq in Q1, much stronger than expectation of 0.5% qoq. Services industries rose 1.1% qoq. Goods producing industries rose 2.4% qoq. Primary industries rose 0.3% qoq. GDP per capita rose 1.5% qoq.

“After an easing of economic activity in the December quarter, we’ve seen broad-based growth in the first quarter of 2021. This is despite Auckland being in alert level 3 lockdown for 10 days, and continued border restrictions,” national accounts senior manager Paul Pascoe said.

Looking ahead

SNB rate decision and Swiss trade balance will be featured in European session. Eurozone will release CPI final. Later in the day, US will release jobless claims and Philly Fed survey. Canada will release ADP employment and foreign securities purchases.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1950; (P) 1.2042; (R1) 1.2090; More…

EUR/USD’s fall from 1.2265 accelerates lower and it’s now pressing 1.1985 support. Sustained break there should confirm that consolidation pattern from 1.2348 is already in the third leg. Deeper decline should be seen to retest 1.1703 support next. On the upside, above 1.2092 minor resistance will turn intraday bias back to the upside for retesting 1.2265 instead.

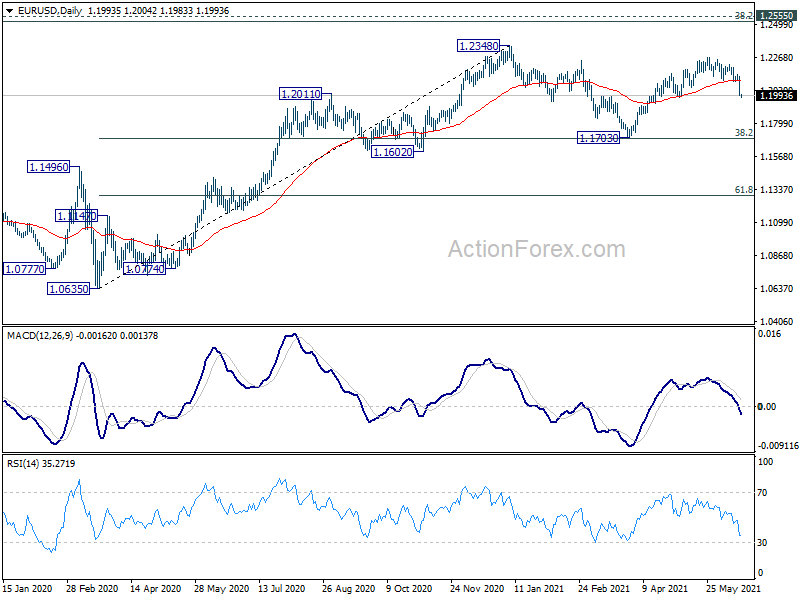

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1602 support holds. Reaction from 1.2555 should reveal underlying long term momentum in the pair. However sustained break of 1.1602 will argue that the rise from 1.0635 is over, and turn medium term outlook bearish again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | GDP Q/Q Q1 | 1.60% | 0.50% | -1.00% | |

| 01:30 | AUD | Employment Change May | 115.2K | 30.0K | -30.6K | -30.7K |

| 01:30 | AUD | Unemployment Rate May | 5.10% | 5.50% | 5.50% | |

| 06:00 | CHF | Trade Balance (CHF) May | 4.23B | 3.84B | ||

| 07:30 | CHF | SNB Interest Rate Decision | -0.75% | -0.75% | ||

| 08:00 | CHF | SNB Press Conference | ||||

| 09:00 | EUR | Eurozone CPI Y/Y May F | 1.60% | 2.00% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y May F | 0.90% | 0.90% | ||

| 12:30 | USD | Initial Jobless Claims (Jun 11) | 360K | 376K | ||

| 12:30 | CAD | ADP Employment Change May | 351.3K | |||

| 12:30 | CAD | Foreign Securities Purchases (CAD) Apr | 4.35B | 3.25B | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Jun | 30.1 | 31.5 | ||

| 14:30 | USD | Natural Gas Storage | 71B | 98B |