The forex markets are generally range bound as traders await FOMC minutes. The main focus will be on discussions on the timing of tapering, which wasn’t clearly indicated in the statement and economic projections. Dollar’s rise appears to be losing steam as global sentiments stabilized today. DOW futures point to a recovery while S&P 500 and NASDAQ might be ready to resume record runs. Commodity currencies are currently the stronger for today while Yen is the weakest.

Technically, we’d reiterate again that Dollar was held below near term levels against most major currencies, despite yesterday’s rally attempt. The levels include 1.1806 support in EUR/USD, 1.3730 support in GBP/USD, 0.7443 support in AUD/USD, 0.9275 resistance in USD/CHF. Return of risk appetite today could push the greenback further away from these levels. Meanwhile, extended weakness in yields could give Yen some support. Happening together, such developments could send USD/JPY through 110.41 short term support decisively.

In Europe, at the time of writing, FTSE is up 0.40%. DAX is up 0.95%. CAC is up 0.03%. Germany 10-year yield is down -0.027 at -0.293. Earlier in Asia, Nikkei dropped -0.96%. Hong Kong HSI dropped -0.40%. China Shanghai SSE rose 0.66%. Singapore Strait Times dropped -1.54%. Japan 10-year JGB yield dropped -0.0097 to 0.037.

IMF: Monetary policy should tighten where inflationary pressures are high

In a note for G20 Finance Ministers and Central Bank Governors’ Meetings later in the week, IMF said that “global growth has progressed broadly in line with projections, with clear signs of divergence.”. It urged “immediate action” by G20 to “arrest the rising human and economic toll of the pandemic”.

Additionally, IMF said policy support should be “tailored to the stage of the crisis, avoiding abrupt transitions.” Monetary policy should “remain accomodative in most economies”. In particular, where “inflation expectations are anchored, ” continued monetary accommodation is warranted”.

However, in economies “furthest ahead in the recovery”, “communicated policy intentions will keep inflation expectations well-anchored and avoid adverse spillovers to weaker economies.” “Where inflationary pressures are high and expectations not firmly anchored, monetary policy should tighten.”

EU and Eurozone growth and inflation forecasts upgrade

In the Summer 2021 Interim Economic Forecast, European Commission upgraded EU and Eurozone GDP growth forecast for 2021 and 2022 respectively. EU GDP growth is projected to be at 4.8% in 2021 (prior 4.2%) and 4.5% in 2022 (prior 4.4%). Eurozone GDP growth is projected to be at 4.8% in 2022 (prior 4.3%) and 4.5% (prior 4.4%).

EU inflation is projected to be at 2.2% in 2021 (prior 1.9%) and 1.6% in 2022 (prior 1.5%). Eurozone inflation is projected to be at 1.9% in 2021 (prior 1.7%) and 1.4% in 2022 (prior 1.3%).

Valdis Dombrovskis, Executive Vice-President for an Economy that Works for People said: “The European economy is making a strong comeback with all the right pieces falling into place. Our economies have been able to reopen faster than expected thanks to an effective containment strategy and progress with vaccinations”

Paolo Gentiloni, Commissioner for Economy said: “The EU economy is set to see its fastest growth in decades this year, fuelled by strong demand both at home and globally and a swifter-than-expected reopening of services sectors since the spring. Thanks also to restrictions in the first months of the year having hit economic activity less than projected.”

Release in European session, Germany industrial production dropped -0.3% mom in may versus expectation of 0.5% mom. France trade deficit widened to EUR -6.8B in May, versus expectation of EUR -6.0B. Italy retail sales rose 0.2% mom in May, versus expectation of 2.3% mom. Swiss foreign currency reserves rose to CHF 941B in June.

Australia AiG services dropped to 57.8, question on filling positions to fill orders

Australia AiG Performance of Services index dropped to 57.8 in June, down from 61.2. Sales dropped -2.5 pts to 66.1. Employment dropped -2.4 pts to 54.2. New orders dropped sharply by -11.7 to 56.6. Input prices dropped -2.7 to 65.4. Selling prices dropped -9.9 to 53.5. Average wages rose 2.9 to 66.0.

Ai Group Chief Executive, Innes Willox, said: “Some adverse impacts on demand and supply chains were associated with the COVID lockdowns and restrictions imposed by other states and territories. Businesses were also constrained by an inability to fill positions required either to maintain existing levels of activity or to expand to meet higher demand. Wages growth accelerated in June and input prices continued to rise although at a more moderate rate than in the previous month. The healthy rise in new orders came on top of the sharp rise in the previous month and points to strong demand over coming months. A key question for many businesses will be whether they can fill positions required to fill these orders.”

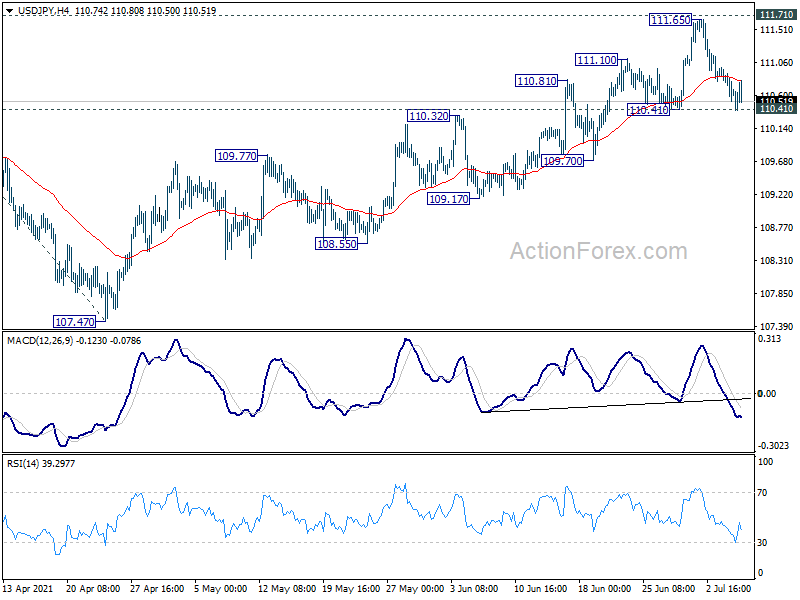

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.43; (P) 110.71; (R1) 110.89; More…

No change in USD/JPY’s outlook and intraday bias remains neutral first. On the downside, firm break 110.41 support will indicate short term topping. Intraday bias will be turned back to the downside for 55 day EMA (now at 109.77). On the upside, sustained break of 111.71 will carry larger implication. Next target is 61.8% projection of 102.58 to 110.95 from 107.47 at 112.64.

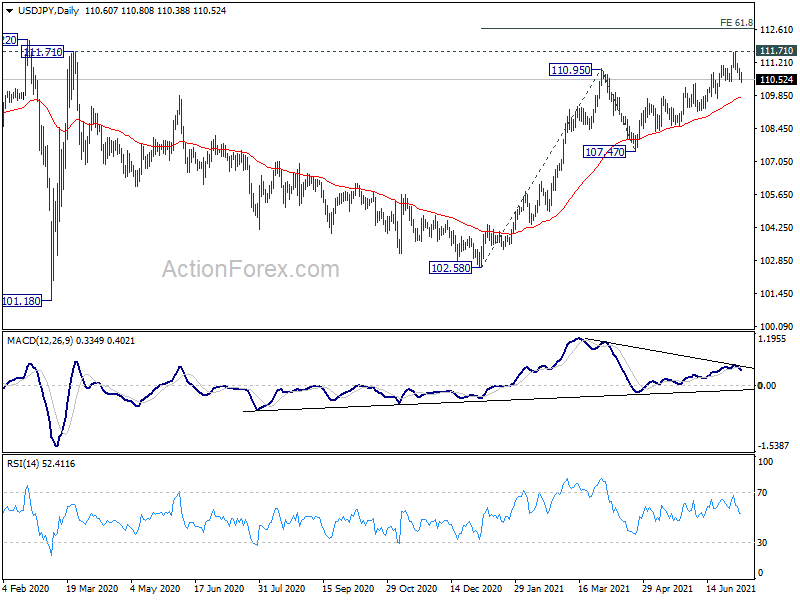

In the bigger picture, medium term outlook is staying neutral with 111.71 resistance intact. Though, as notable support was seen from 55 day EMA, rise from 102.58 is mildly in favor to extend higher. Decisive break of 111.71/112.22 resistance will suggest medium term bullish reversal. Rise from 101.18 could then target 118.65 resistance (Dec 2016) and above. However, sustained break of 55 day EMA would revive some medium term bearishness, and open up deep fall to 61.8% retracement of 102.58 to 110.95 at 105.77 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Services Index Jun | 57.8 | 61.2 | ||

| 5:00 | JPY | Leading Economic Index May P | 102.6 | 103.5 | 103.8 | |

| 6:00 | EUR | Germany Industrial Production M/M May | -0.30% | 0.50% | -1.00% | -0.30% |

| 6:45 | EUR | France Trade Balance (EUR) May | -6.8B | -6.0B | -6.2B | |

| 7:00 | CHF | Foreign Currency Reserves (CHF) Jun | 941B | 902B | ||

| 8:00 | EUR | Italy Retail Sales M/M May | 0.20% | 2.30% | -0.40% | -0.10% |

| 9:00 | EUR | EU Economic Forecasts | ||||

| 14:00 | CAD | Ivey PMI Jun | 65 | 64.7 | ||

| 18:00 | USD | FOMC Minutes |