Dollar weakens in early US session, in particular against Yen. PCE inflation showed notable acceleration in May but fell short of expectations slightly. Nevertheless, Sterling is the worst performing ones for today, extending post BoE selloff. The Pound is also pressured by uncertainties over resurgence of coronavirus infections. Commodity currencies are the strongest, as US futures point to extending record run.

Technically, EUR/GBP’s breach of 0.8600 resistance is the first sign that choppy decline from 0.8718 has completed. We’d not see if there is any follow through buying to push it through 0.8670 resistance to confirm. At the same time, GBP/USD is struggling in range below 1.4000 resistance and 4 hour 55 EMA. We’d also see if selloff in Sterling would push it through 1.3859 minor support. Or, the selloff in Dollar would push GBP/USD through 1.4000.

In Europe, at the time of writing, FTSE is up 0.36%. DAX is down -0.05%. CAC is down -0.09%. Germany 10-year yield is up 0.0139 at -0.172. Earlier in Asia, Nikkei rose 0.66%. Hong Kong HSI rose 1.40%. China Shanghai SSE rose 1.15%. Singapore Strait Times rose 0.06%. 10-year JGB yield dropped -0.0030 to 0.051.

US PCE rose to 3.9% yoy in May, core PCE rose to 3.4% yoy

US personal income dropped -2.0% mom, or USD 414.3B in May matched expectations. The fall in personal income primarily reflected a decrease in government social benefits. Spending dropped -0.4% mom, also matched expectations. Headline PCE price index accelerated to 3.9% yoy, up from 3.6% yoy, below expectation of 4.0% yoy. Core PCE price index accelerated to 3.4% yoy, up from 3.1% yoy, missed expectation of 3.5% yoy.

Germany Gfk consumer sentiment rose to -0.3, leaving the lockdown behind more and more

Germany Gfk consumer sentiment for July improved to -0.3, up from -6.9. That’s the best level since August 2020. For June, economic expectations rose from 41.1 to 58.4, highest since February 2011. Income expectations rose from 19.5 to 34.1, highest since February 2020. Propensity to buy rose from 10.0 to 13.4.

Rolf Bürkl, GfK consumer expert comments on the subject: “We are leaving the lockdown behind more and more. Sharply declining incidence rates, as well as significant progress in vaccination, allow increasingly extensive relaxations or openings. In addition, vacation travel is now possible again. This leads to increased optimism, which is also reflected in improved consumer confidence. As a result, we are forecasting a value of -0.3 points in consumer sentiment for July 2021, the highest value since the summer of last year. A higher value was last measured in August 2020, at -0.2 points.”

From Eurozone, M3 money supply rose 8.4% yoy in May, below expectation of 8.5% yoy.

UK Gfk consumer confidence unchanged at -9, upwards trajectory still on track

UK Gfk consumer confidence was unchanged at -9 in June, below expectation of -7. Joe Staton, Client Strategy Director GfK, says: “While the shifting sands of an end to lockdown might be the closest most of us get to a summer beach holiday, consumer confidence remains stable at -9 after 16 months of a COVID-induced roller-coaster. A repetition of last month’s score doesn’t mean confidence is about to nose-dive. The upwards trajectory for the Index since the dark days at the start of the pandemic is currently still on track.”

New Zealand exports rose 8.5% yoy in May, imports jumped 31% yoy

New Zealand goods exports rose NZD 461m, or 8.5% yoy, to NZD 5.9B in May. Goods imports rose NZD 1.3B, or 31% yoy, to NZD 5.4B. Trade surplus came in at NZD 469m, up from NZD 414m.

Imports from all top trading partners were up, including China (+9.4% yoy), EU (+28% yoy), Australia (+23% yoy), USA (+34% yoy), and Japan (+103% yoy. Exports to all top trading partners were up expect Australia, including China (+25% yoy), Australia (-13% yoy), USA (+11% yoy), EU (+22% yoy), and Japan (+3.5% yoy).

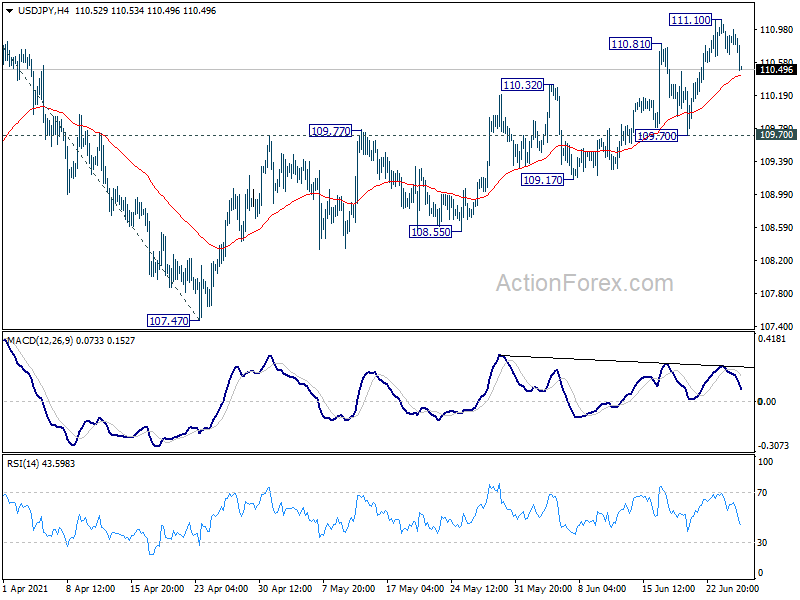

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.67; (P) 110.90; (R1) 111.10; More…

Intraday bias in USD/JPY is turned neutral with current retreat. But further rise remains in favor with 109.70 support intact. Above 111.10 will target 111.71 key resistance. Firm break there will carry larger implication. Next target is 61.8% projection of 102.58 to 110.95 from 107.47 at 112.64 next. On the downside, however, break of 109.70 support will turn bias back to the downside for 107.47 support instead.

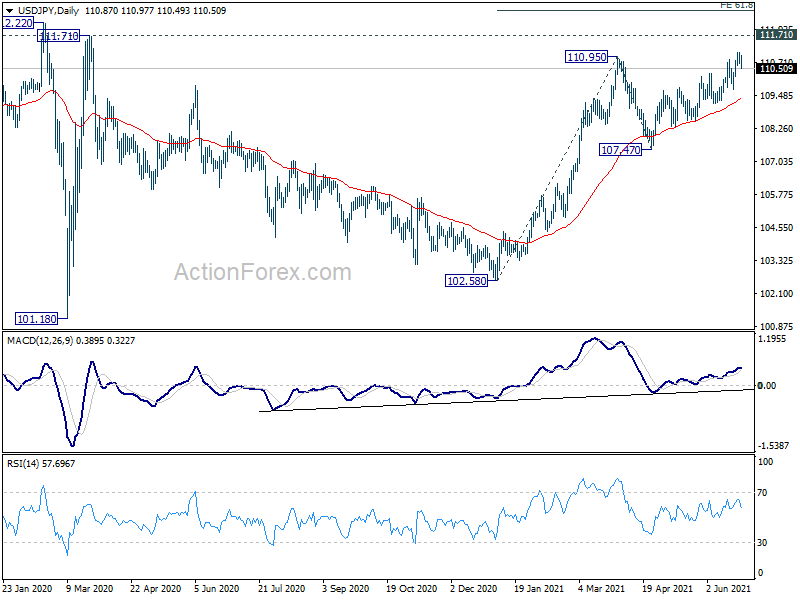

In the bigger picture, medium term outlook is staying neutral with 111.71 resistance intact. On the upside, decisive break of 111.71/112.22 resistance will suggest medium term bullish reversal. Rise from 101.18 could then target 118.65 resistance (Dec 2016) and above. However, sustained break of 107.47 support would revive some medium term bearishness, and open up deep fall to 61.8% retracement of 102.58 to 110.95 at 105.77 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) May | 469M | 388M | 414M | |

| 23:01 | GBP | GfK Consumer Confidence Jun | -9 | -7 | -9 | |

| 23:30 | JPY | Tokyo CPI core Y/Y Jun | 0.00% | -0.10% | -0.20% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence Jul | -0.3 | -4 | -7 | -6.9 |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y May | 8.40% | 8.50% | 9.20% | |

| 12:30 | USD | Personal Income M/M May | -2% | -2.00% | -13.10% | |

| 12:30 | USD | Personal Spending M/M May | 0.40% | 0.40% | 0.50% | 0.90% |

| 12:30 | USD | PCE Price Index M/M May | 0.00% | 0.30% | 0.60% | |

| 12:30 | USD | PCE Price Index Y/Y May | 3.90% | 4.00% | 3.60% | |

| 12:30 | USD | Core PCE Price Index M/M May | 0.50% | 0.60% | 0.70% | |

| 12:30 | USD | Core PCE Price Index Y/Y May | 3.40% | 3.50% | 3.10% | |

| 14:00 | USD | Michigan Consumer Sentiment Index Jun | 86.4 | 86.4 |