Euro is once again capturing market attention today as this week’s significant selloff resumes. The steep decline has been driven by rising political tensions in France, as the snap parliamentary election called by President Emmanuel Macron has heightened investor anxiety, particularly as left-wing parties coalesce against him. There is a growing concern among market participants that the far-right, led by Marine Le Pen’s National Rally, could secure a victory and promote a high-spending agenda, exacerbating France’s already substantial debt burden.

This political uncertainty has triggered safe-haven flows towards German bonds, resulting in a drop in German benchmark yields while French yields have remained steady. Consequently, the spread between French and German borrowing costs is on course for its largest weekly increase since Eurozone debt crisis in 2011, and hit the highest level in four years. French stock market, represented by CAC 40, has also suffered, reaching its lowest level since January.

In parallel, Yen has managed to recover from its post-BoJ losses. BoJ Governor Ueda attempted to reassure markets by confirming that bond purchase tapering would commence in July, with the reduction expected to be “significant.” However, Ueda stressed the importance of maintaining flexibility to ensure market stability. Meanwhile, he also suggested that interest rate adjustments could be possible in July based on upcoming economic and price data.

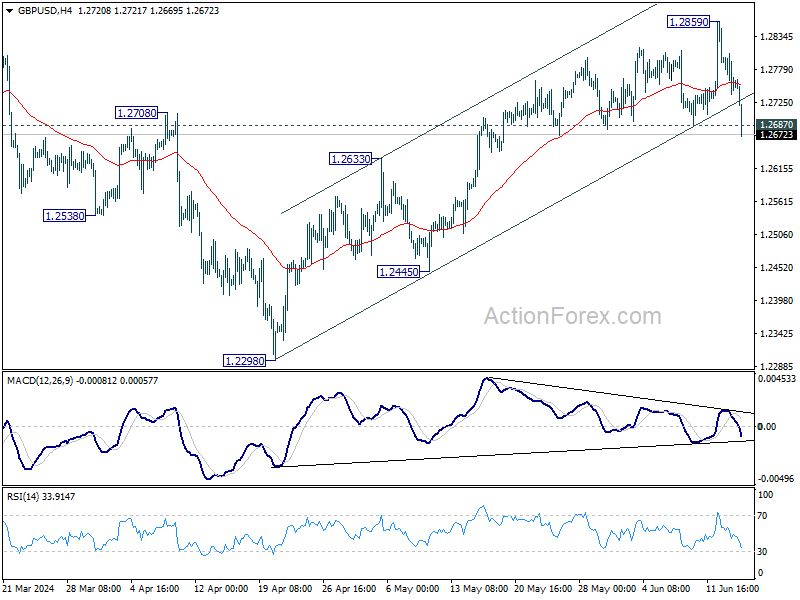

Technically, GBP/USD’s break of 1.2687 support argues that rise from 1.2298 might have completed at 1.2859, on bearish divergence condition in 4H MACD. Firm break of 1.2633 resistance turned support will pave the way to 1.2445 next.

As the GBP/USD continues its decline, it will also be crucial to monitor whether AUD/USD breaks 0.6575 support and whether USD/CAD surpasses 1.3790 resistance, which would confirm underlying strength in Dollar.

In Europe, at the time of writing, FTSE is down -0.04%. DAX is down -1.18%. CAC is down -2.17%. UK 10-year yield is down -0.0589 at 4.070. Germany 10-year yield is down -0.104 at 2.370. Earlier in Asia, Nikkei rose 0.24%. Hong Kong HSI fell -0.94%. China Shanghai SSE rose 0.12%. Singapore Strait Times fell -0.81%. Japan 10-year JGB yield fell -0.0339 to 0.938.

Eurozone exports rises 14.0% yoy, imports up 1.8% yoy in Apr

Eurozone goods exports rose 14.0% yoy to EUR 247.6B in April. Goods imports rose 1.8% yoy to EUR 232.5B. Trade balance showed EUR 15.0B surplus. Intra-Eurozone trade rose 5.8% yoy to EUR 222.89B.

In seasonally adjusted term, goods exports rose 3.1% mom to EUR 245.3B. imports rose 2.3% mom to EUR 225.9B. Trade balance reported EUR 19.4B surplus, above expectation of EUR 17.0B. Intra-Eurozone trade rose 1.5% mom to EUR 217.7B.

BoJ holds interest rates, prepares for bond purchase reduction plan in next month

BoJ left uncollateralized overnight call rate unchanged at 0-0.10% as widely expected. In addition, BoJ will continue its asset purchase program until the end of June. The central bank, by an 8-1 majority vote, has also decided to reduce its JBG purchase amounts afterward.

The detailed plan for the reduction in JGB purchases, which will cover the next one to two years, is set to be determined by at next meeting. Apparently, BoJ would likely to have access to the new economic and price output report before laying out the plan.

BoJ is optimistic about Japan’s economic prospects, projecting that the economy will grow at a rate above its potential growth rate. Core CPI is expected to increase through fiscal 2025 due to factors such as the waning effects of government economic measures. Furthermore, underlying inflation is predicted to gradually rise as the output gap improves and medium-to long-term inflation expectations climb.

NZ BNZ manufacturing falls to 47.2 in 15th month of contraction

New Zealand’s BusinessNZ Performance of Manufacturing Index dropped from 48.8 to 47.2 in May, marking the sector’s 15th consecutive month of contraction.

Looking as some details, production plummeted from 50.3 to 44.5, indicating a sharp return to contraction. Employment showed a slight decline from 50.9 to 50.6. New orders fell further from 45.4 to 44.4, maintaining their contraction for the 21st straight month. Finished stocks rose from 50.7 to 52.4, but deliveries fell from 48.1 to 45.2.

Despite the decline in the overall index, the proportion of negative comments decreased to 63.5% from 69% in April and 65% in March. Most negative feedback highlighted the general economic slowdown and the current recessionary pressures.

EUR/USD Mid-Day Outlook

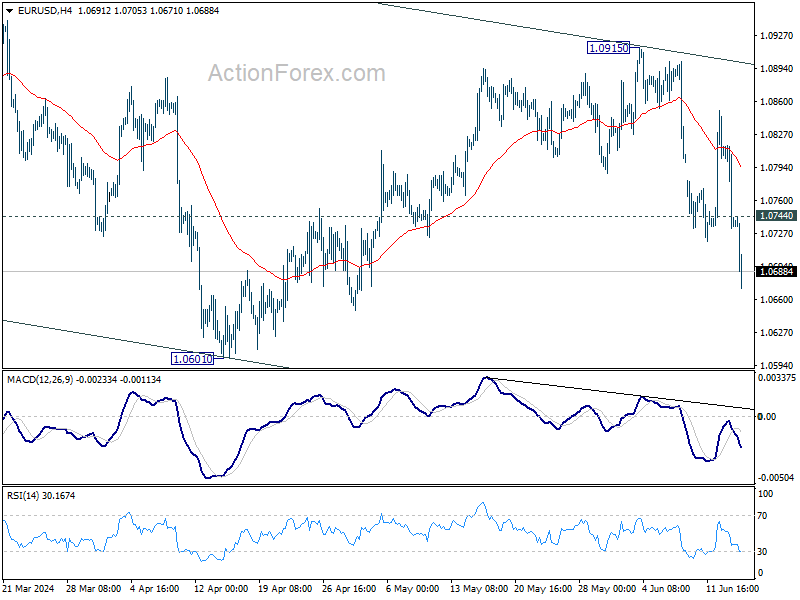

Daily Pivots: (S1) 1.0709; (P) 1.0763; (R1) 1.0793; More….

Intraday bias in EUR/USD continues today and intraday bias stays on the downside for 1.0601 support. Firm break there will resume whole decline from 1.1138, as the third leg of the pattern from 1.1274, and target channel support at 1.0510. On the upside, above 1.0744 minor resistance will turn intraday bias neutral again first.

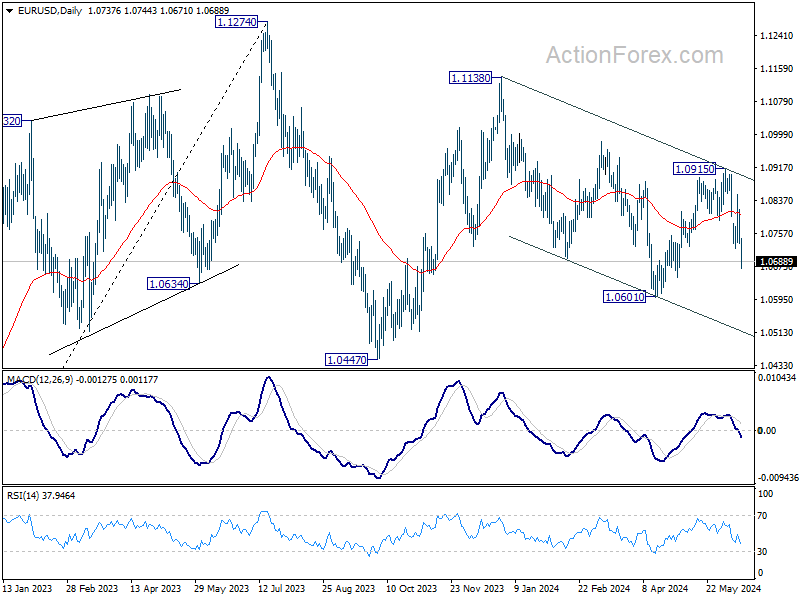

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, which might still be in progress. Break of 1.0601 will target 1.0447 support and possibly below. Nevertheless, on the upside, firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI May | 47.2 | 48.9 | 48.8 | |

| 03:23 | JPY | BoJ Interest Rate Decision | 0.10% | 0.10% | 0.10% | |

| 04:30 | JPY | Tertiary Industry Index M/M Apr | 1.90% | 0.40% | -2.40% | -2.30% |

| 04:30 | JPY | Industrial Production M/M Apr F | -0.90% | -0.10% | -0.10% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Apr | 19.4B | 17.0B | 17.3B | 17.2B |

| 12:30 | CAD | Manufacturing Sales M/M Apr | 1.10% | 1.30% | -2.10% | |

| 12:30 | CAD | Wholesale Sales M/M Apr | 2.40% | 2.50% | -1.10% | -1.30% |

| 12:30 | USD | Import Price Index M/M May | -0.40% | 0.10% | 0.90% | |

| 14:00 | USD | Michigan Consumer Sentiment Index Jun P | 73 | 69.1 |