Being the first Friday of the month, the day sorta felt like it should have been an employment day. However, because of the quirks of the shortened calendar month of February, this Friday was void of the big job report. That data will have to wait until next week, when both the US and Canada jobs reports will be released (and it will be 10th of the month).

We did get the ISM non-manufacturing data today which came in better than expectations at 55.1 vs 54.5. Within that report was the the employment component which came in higher at 54.0 versus 49.8 expected and 50.0 last month (so there was some jobs data afterall). That was a better reading than the manufacturing employment component released on Wednesday which had the employment component declining to 49.1 from 50.6 last month. New orders were also strong at 62.6 versus 58.5 expected. The prices paid index fell from 67.8 to 65.6 but it was still higher than the 64.5 expected, and still way above the 50.0 level.

The strong data helped to send the dollar back to the upside (it was the weakest of the majors coming into the trading session).

However, after treasury yields initially moved higher, the momentum stalled and yields started to rotate back to the downside. The 10 year yield fell back below the key 4% level and then the 100 hour moving average (at 3.982%). The 200 hour moving average at 3.962% was approached going into the close. That moving average level will be a key barometer in the new trading week.

Meanwhile, US stocks, were encouraged by the declining yields as well. As a result, they too started to rally. The NASDAQ index led the charge with a gain of 1.97% which was the best day since February 2. The S&P increase by 1.62% which was its best day since January 6.

For the trading week all the major indices snatch victory from the jaws of defeat from earlier this week when the prices were reaching new corrective lows and breaking below some key technical levels including the 200 day MA in both the S&P and Nasdaq indices.

For the trading week, the

- NASDAQ gained 2.58%,

- S&P rose by 1.9%, and the

- Dow Industrial Average rose by 1.75%.

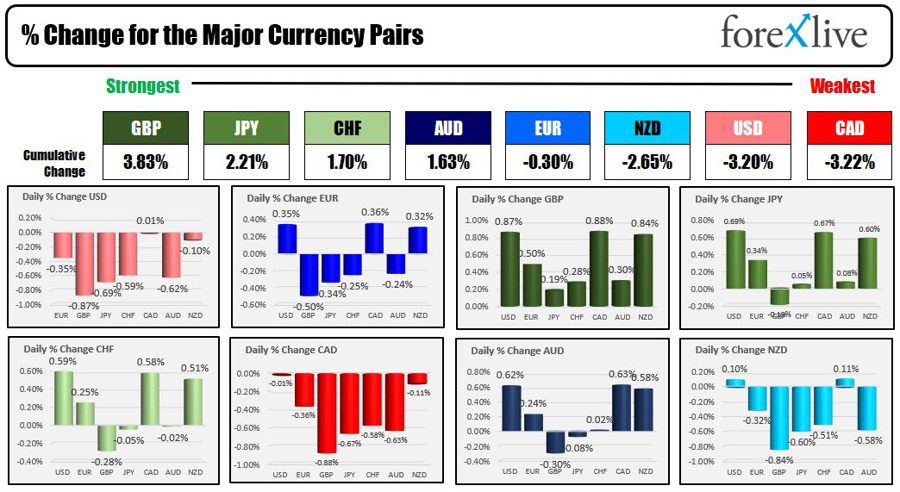

IN the forex market, the GBP is ending the day as the strongest of the majors. The weakest was the a virtual tie between the USD and the CAD. The dollar fell -0.87% vs the GBP and -0.69% vs the JPY.

The strongest to the weakest of the major currencies

For the trading week, the USD was lower vs all the major currencies although the changes were fairly modest. It moved the most vs the NZD. Against that currency the decline was still less than 1.0% at -0.96%. Versus the CAD, the greenback was only lower by 0.07% (just about 9 pips from the close a week ago):

- -0.82% vs the EUR

- -0.48% vs the JPY

- -0.88% vs the GBP

- -0.45% vs the CHF

- -0.07% vs the CAD

- -0.66% vs the AUD

- -0.96% vs the NZD

IN other markets:

- Spot gold was encouraged by the lower yields in lower dollar and rallied $19.72 today or 1.07% to $1855.19. For the week, spot gold increase by $45.31 or 2.5%

- spot silver is closing higher by $0.35 or 1.68% at $21.23. For its week, in the $0.48 or 2.31%

- WTI crude oil is trading near the high for the week at $79.82. That is up $1.66 or 2.11% today. For the trading week, crude oil is up $3.49 or 4.57%

- Bitcoin did not have a risk on flow today as the Silvergate news this week pressured the digital currency. The prices trading at $22,279. For the trading week, the prices down once $1283 or -5.45%.

In the US debt market:

- 2 year yield is trading at 4.86%. This week the yield reached 4.944% which was the highest level going back to July 2007. However, yields backed off and for the week it is still ending up but only by 4.1 basis points

- 10 year yield is at 3.959% which is down -11 basis points on the day. The high-yield this week reached 4.089%. For the trading week, the yield is up only 1.1 basis points

- 30 year yield is at 3.877% which is down -14 basis points on the day. The high yield reached 4.047% this week. For the trading week yield fell -5.7 basis points

In the new trading week, in addition to the employment report on Friday, other employment measures including the ADP jobs report, the JOLTS job openings, and the Challenger jobs survey will be released.

In addition, Fed Chair Powell will be testifying on Capitol Hill on both Tuesday and Wednesday. The market will be keen to his views on whether his playbook remains intact or has been ratcheted up a notch as a result of the stronger data. There were some Fed officials this week who seem to be leaning higher, and others that seem to be satisfied with the current playbook of getting the rate toward 5.25% and sitting still for an extended period time.

The Fed funds futures for October delivery reached an implied yield of around 5.50% this week before settling at 5.455%. The Federal Reserve will announce their next rate decision on March 22.

Thank you for all your support this week. Hope you have a good weekend.