After a brief recovery, risk sentiment turned sour again towards the end of the week. Solid data from the US that solidify expectation for continuous aggressive Fed actions was a factor. Strong rebound in oil price also raised concern of a second wave in inflation. The overall development suggests that risk sentiment remains fragile, and extended selloff in stocks and bonds ahead could give Dollar further boost ahead.

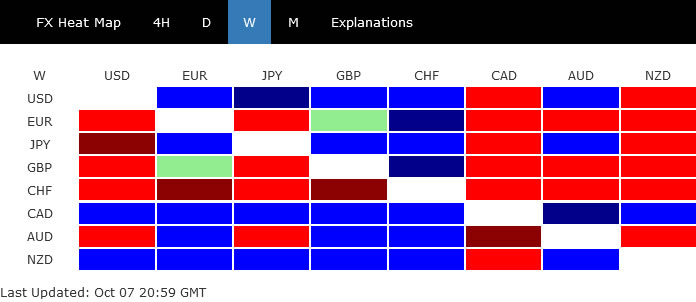

Dollar did rally broadly towards the end of the week, but that wasn’t enough to push it through near term resistance levels against most major rivals. Greenback buyers were probably still on the sideline, awaiting upcoming inflation data. Indeed, Canadian Dollar eked out the first place for its resilience, while New Zealand Dollar was second only because of its earlier gains. Swiss Franc was the worst performer, followed by Euro and Sterling.

Robust job data backs more aggressive Fed tightening

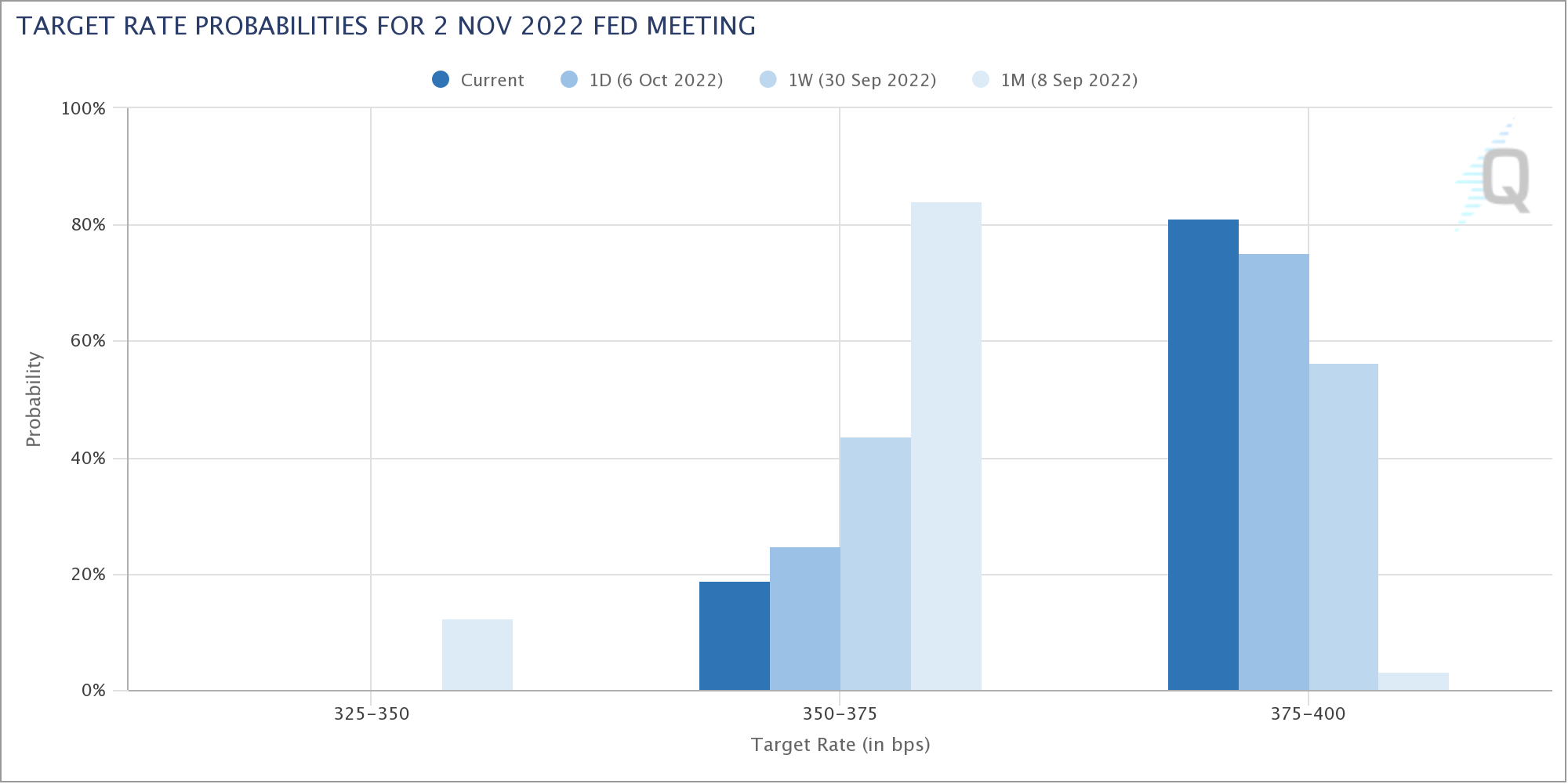

Comments from Fed officials last week indicate that the majority are still leaning towards continuing the tightening pace. Their views were backed up by a set of robust non-farm payroll data. ISM indexes showed while there was some slowdown in manufacturing, services remained resilient. Fed fund futures are pricing in 81% chance of another 72bps hike on November 2 to 3.75-4.00%, comparing to just 56% a week ago. The upcoming September CPI data is crucial to solidify such expectations.

Oil rebounded strongly after OPEC+ pre-emptive production cut

Strong rebound in oil price was another factor that investors could find worrying. OPEC+ announced its largest supply cut since 2020. OPEC and allies including Russia agreed to lower output target by 2 million bpd, equalling to 2% of global supply. OPEC Secretary General Haitham al-Ghais said there’s a “high possibility that recession will happen”, and the decisions was “pre-emptive”. EU also agreed to impose a price cap of Russian oil, which will squeeze supply further.

WTI crude oil closed strongly at 96.97, taking out 55 day EMA decisively. Further rise is now in favor to 38.2% retracement of 130.50 to 76.25 at 96.97 and possibly above. But overall market sentiment could stay relatively calm as long as it stays below 100 psychological level.

Yet, given that correction from 130.50 has possibly completed with three waves down to 76.25, decisive break of 100 could push WTI further to 61.8% retracement at 109.78, which is close to 110. If that happens, sentiment should be dashed further by prospect of more prolonged inflation, higher terminal interest rates, and a longer time monetary policy stays restrictive.

S&P 500 ready for down trend resumption after brief recovery

Despite a strong start, US stocks reversed and pared back most of earlier gains to close a a very weak note. S&P 500’s brief recovery indicates that outlook stays bearish and the corrective down trend from 4818.62 might be ready to resume soon. Break of 3584.13 support will confirm and target 100% projection of 4818.62 to 3636.87 from 4325.28 at 3143.53. The power of the downside breakout would depend on the US inflation data as well as development in oil prices.

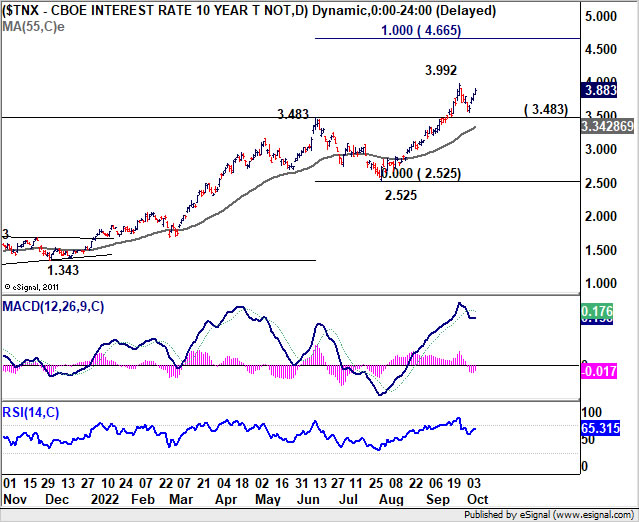

US 10-year yield to take on 4% handle again soon

US 10-year yield’s retreat from 3.992 might have completed after last week’s rebound. Such retreat now looks more likely just a near term correction than not. And even in case of another fall, 3.483 resistance turned support should provide a floor. Break of 3.992 will resume up trend through 4% psychological level to 100% projection of 1.343 to 3.483 from 2.525 at 4.665. Such development, if happens, will reconfirm worries on prolonged inflation and tightening.

Dollar index staying bullish, but upside breakout not warranted yet

Dollar’s reaction to NFP was affirmative to its underlying bullishness, but somewhat disappointing. The greenback could only break through recent high against Aussie, but stuck in range against others. Outlook in Dollar index remains clearly bullish as it’s holding well above 55 day EMA (now at 109.36) as well as medium term channel support. But current upside momentum doesn’t warrant a breakout yet.

Still, in case of of another fall, strong support should be seen from 55 day EMA to contain downside. Break of 114.77 will resume larger up trend to 100% projection of 94.62 to 109.29 from 104.63 at 119.30. In this case, there is prospect of upside acceleration if risk aversion intensifies while 10-year yield breaks 4%.

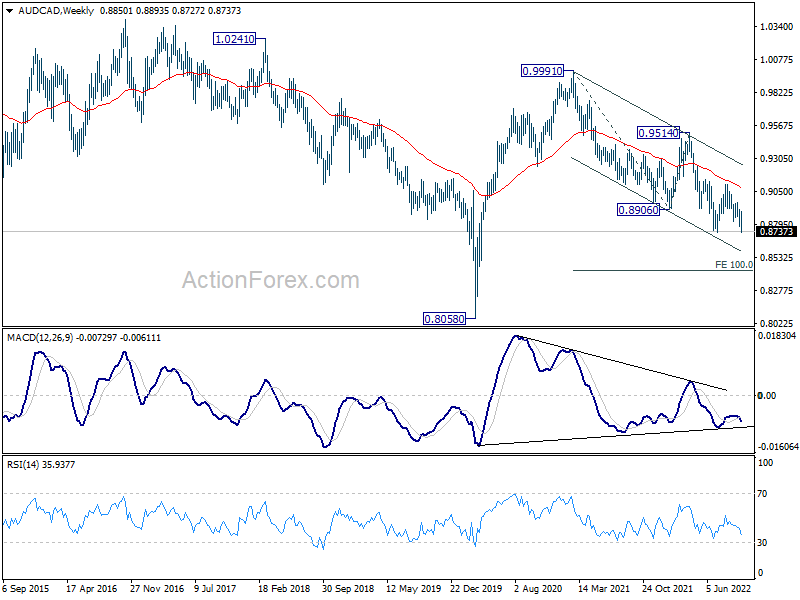

AUD/CAD breakout on BoC and RBA divergence

Canadian Dollar was support by rebound in oil price, solid job data, as well as hawkish comments from BoC Governor Tiff Macklem. Macklem indicated that more work is needed to be done to curb inflation, and it’s too soon to take a “decision-by-decision” approach to monetary policy. That is, another 75bps hike is on the card for October 26 meeting.

On the other hand, RBA has already started slowing down tightening, and delivered only a 25bps hike last week. It’s likely continue to lag behind others in pace.

AUD/CAD breached 0.8733 support last week as down trend is now ready to resume. Further decline is expected as long as 0.8874 resistance holds. Next near term target is 61.8% projection of 0.9514 to 0.8733 from 0.9104 at 0.8621.

Sustained break of 0.8621, coupled with further divergence in monetary policy between BoC and RBA, could send AUD/CAD to medium term target of 100% projection of 0.9991 to 0.8906 from 0.9514 at 0.8429, with downside acceleration.

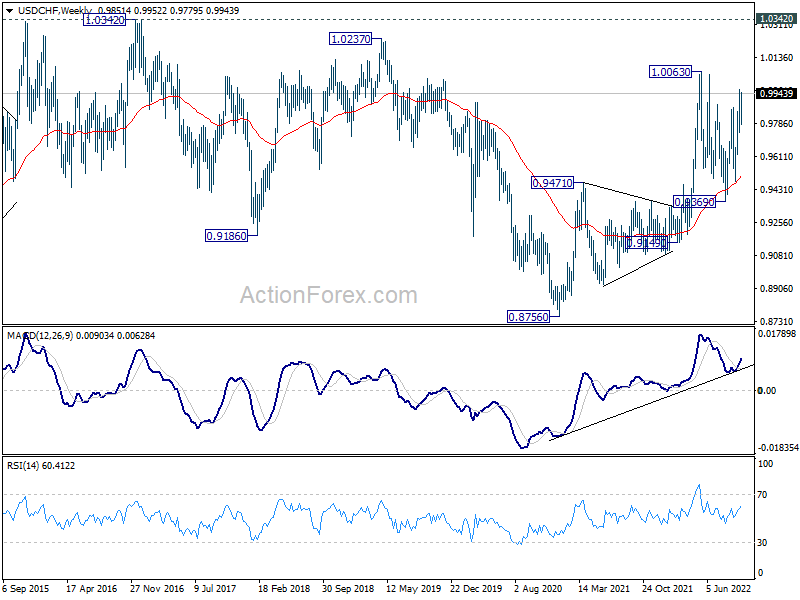

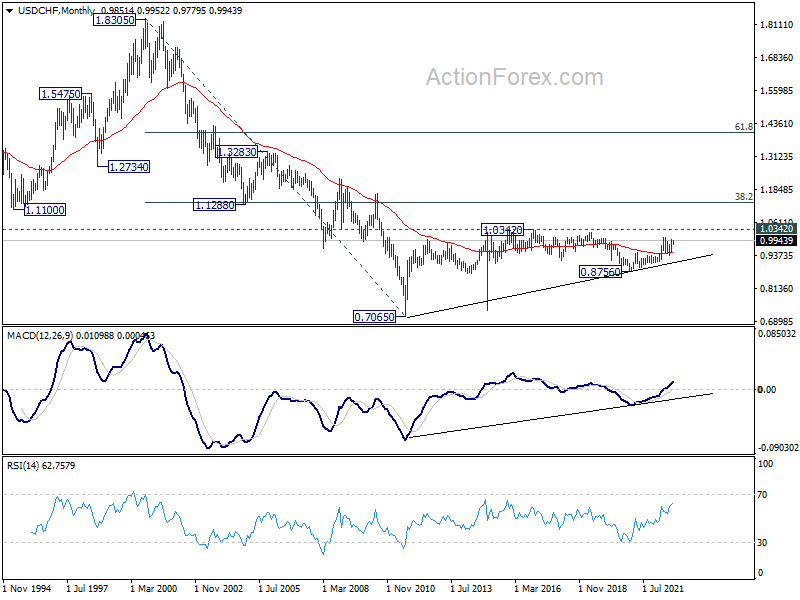

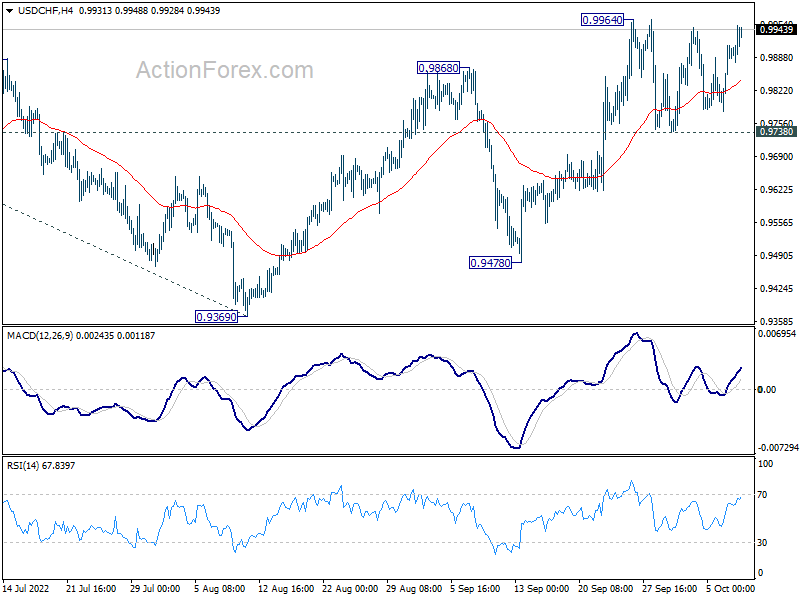

USD/CHF Weekly Outlook

USD/CHF stayed in consolidation from 0.9964 last week and outlook is unchanged. Initial bias remains neutral this week first. On the upside, above 0.9964 will resume the rally from 0.9369 to retest 1.0063 high. For now, outlook will stay bullish as long as 0.9738 support holds, in case of retreat.

In the bigger picture, current development suggests that up trend from 0.8756 (2021 low) is still in progress. Sustained break of 1.0063 will target 100% projection of 0.9149 to 1.0063 from 0.9369 at 1.0283, and then 1.0342 (2016 high). For now, this will remain the favored case as long as 0.9369 support holds, even in case of deep pull back.

In the long term picture, outlook is mixed with deeper than expected fall from 1.0063, but some support was seen from 55 week EMA (now at 0.9492). Overall, though, USD/CHF is seen as in sideway pattern from 1.0342 (2016 high). Range trading should continue until further development.