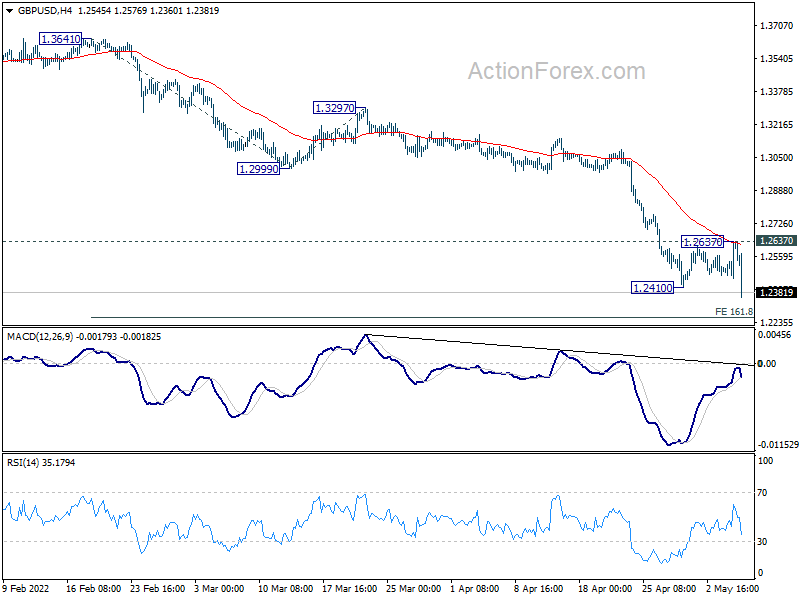

Sterling drops sharply today even after BoE raised interest rate as expected. The trigger was the warning that of recession as high inflation hurts real incomes of household and profits of businesses. Aussie and Kiwi are also trading lower as yesterday’s risk-on rally fades. Dollar, on the other hand, is regaining some of the post FOMC losses. As for the week, though, Sterling is the worst so far, followed by Franc. Aussie is still the strongest, followed by Loonie.

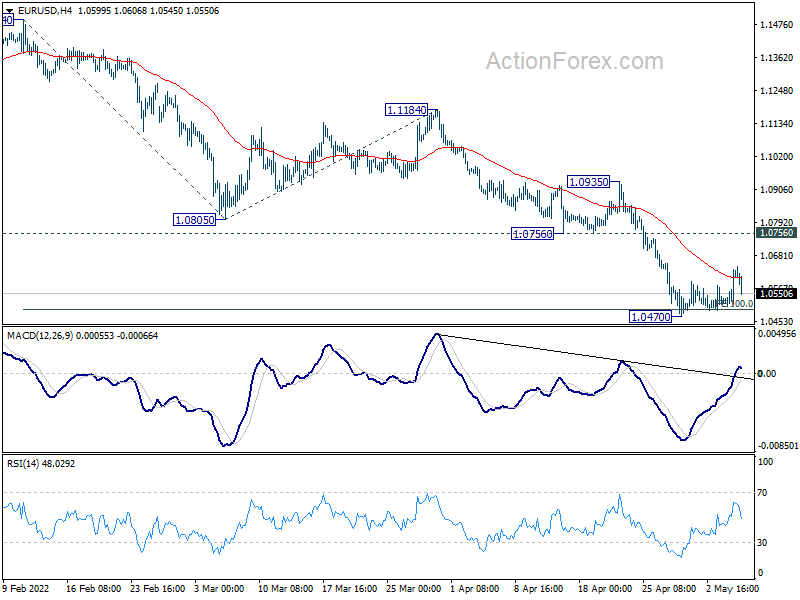

Technically, the development in Sterling is rather bad, with GBP/USD breaking through 1.2410 support to resume medium term down trend. EUR/GBP’s strong break of 0.8511 resistance reaffirms that it’s in medium term rebound. A focus now is indeed on whether Euro will also follow. Hence, attention will be back on 1.0470 support in EUR/USD.

In Europe, at the time of writing, FTSE is up 1.58%. DAX is up 1.56%. CAC is up 1.90%. Germany 10-year yield is down -0.0045 at 0.928. Earlier in Asia, Japan was on holiday. Hong Kong HSI dropped -0.36%. China Shanghai SSE rose 0.68%. Singapore Strait Times dropped -0.17%.

US initial jobless claims rose to 176k, continuing claims dropped to 1.384m

US initial jobless claims rose 19k in the week ending April 30, above expectation of 176k. Four-week moving average of initial claims rose 8k to 188k.

Continuing claims dropped -19k to 1384k in the week ending April 23, lowest since January 17, 1970. Four-week moving average of continuing claims dropped -36k to 1417k, lowest since February 21, 1970.

BoE hikes by 25bps, three MPC members wanted 50bps

BoE raises Bank Rate by 25bps to 1.00% as widely expected. The decision was made by 6-3 vote, with three members voted for 50bps hike, including Jonathan Haskel, Catherine Mann and Michael Saunders.

In the accompany statement, BoE reaffirmed its preference that the Bank Rate will be used as the active policy tool in adjusting monetary policy stance. It will “consider” beginning the process of selling the assets purchased., but the decision will depend on economic circumstances. The strategy on offloading the assets will be provided at the August meeting.

BoE also updated the economic projections conditions on a market-implied path for Bank Rate that rises to around 2.50% by mid-2023, before falling to 2.00% at the end of the forecast period. CPI is expected to rise further over the remainder of the year, averaging slightly over 10% at its peak in 2022 Q4, then falls back to 2% target in around two years. GDP is projected to fall in 2022 Q4 and calendar year GDP growth is broadly flat in 2023.

UK PMI services finalized at 58.9, twin headwinds of costs and war

UK PMI Services was finalized at 58.9 in April, down from March’s 62.6. S&P Global noted that input cost inflation hit fresh record high. Activity and new business continued to rise, but a reduced rates. Business confidence was lowest in a year-and-a-half. PMI Composite was finalized at 58.2, down from March’s 60.9.

Andrew Harker, Economics Director at S&P Global: “The twin headwinds of the cost of living crisis and the war in Ukraine started to bite on the UK service sector during April, as evidenced by a sharp slowdown in new order growth to the lowest in the year so far. Worryingly, companies seem to be expecting impacts to be prolonged, with business confidence dropping to the lowest in a year-and-a-half.”

ECB Lane: Gradualism is an important consideration in thinking about normalization

ECB Chief Economist Philip Lane said in a speech, “in thinking about the normalization process, gradualism is an important consideration.” There are two basic reasons that make the timeline of completing normalization “intrinsically uncertain”.

Firstly, “the feedback loop between various steps in the policy normalisation process and inflation dynamics needs to be incorporated into the monetary policy decision process”.

Secondly, “high uncertainty about the economic impact of the war in Ukraine, the energy shock and the post-pandemic recovery suggests that it is unlikely that the economy will quickly settle into a new steady-state equilibrium.”

Lane reiterated that the calibration of policies will “will remain data-dependent and reflect our evolving assessment of the outlook”.

Released in European session, Germany factory orders dropped -4.7% in March versus expectation of -0.5%. France industrial output dropped -0.5% mom in March versus expectation of 0.0% mom. Swiss CPI came in at 0.4% mom, 2.5% yoy in April, versus expectation of 0.2% mom, 2.5% yoy.

China Caixin PMI services dropped to 36.2 in Apr, PMI composite down to 37.2

China Caixin PMI Services dropped from 42.0 to 36.2 in April, below expectation of 40.9. That’s the second straight month of steep decline, and the worst reading since February 2020. Caixin said decline in new business gathered pace but employment fell only slightly. PMI Composite dropped from 43.9 to 37.2, also the worst since the onset of the pandemic.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Overall, in April, local Covid outbreaks continued and activity in the manufacturing and service sectors continued to contract, with services shrinking more. Demand was under pressure, external demand deteriorated, supply shrank, supply chains were disrupted, delivery times were prolonged, backlogs of work grew, workers found it difficult to return to their jobs, inflationary pressures lingered, and market confidence remained below the long-term average.”

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2513; (P) 1.2575; (R1) 1.2699; More…

GBP/USD’s down trend resumes by breaking through 1.2410 support. Intraday bias is back on the downside for 161.8% projection of 1.3641 to 1.2999 from 1.3297 at 1.2258. Break will target 200% projection at 1.2013 next. On the upside, break of 1.2637 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, rise from 1.1409 (2020 low) has completed at 1.4248, ahead of 1.4376 long term resistance (2018 high). Based on current momentum, fall from 1.4248 is probably the start of a long term down trend. The break of 61.8% retracement of 2.1161 to 1.1409 at 1.2493 is affirming this bearish case too. For now, deeper decline would be seen as long as 1.3158 support turned resistance holds. Next target is 1.1409 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Building Permits M/M Mar | -18.50% | -12.00% | 43.50% | 42.00% |

| 01:30 | AUD | Trade Balance (AUD) Mar | 9.31B | 7.80B | 7.46B | 7.44B |

| 01:45 | CNY | Caixin Services PMI Apr | 36.2 | 40.9 | 42 | |

| 06:00 | EUR | Germany Factory Orders Mar | -4.70% | -0.50% | -2.20% | -0.80% |

| 06:30 | CHF | CPI M/M Apr | 0.40% | 0.20% | 0.60% | |

| 06:30 | CHF | CPI Y/Y Apr | 2.50% | 2.50% | 2.40% | |

| 06:45 | EUR | France Industrial Output M/M Mar | -0.50% | 0.00% | -0.90% | |

| 08:30 | GBP | Services PMI Apr F | 58.9 | 58.3 | 58.3 | |

| 11:00 | GBP | BoE Interest Rate Decision | 1.00% | 1.00% | 0.75% | |

| 11:00 | GBP | MPC Official Bank Rate Votes | 9–0–0 | 8–0–1 | 8–0–1 | |

| 11:30 | USD | Challenger Job Cuts Y/Y Apr | 6.00% | -30.10% | ||

| 12:30 | USD | Initial Jobless Claims (Apr 29) | 200K | 176K | 180K | 181K |

| 12:30 | USD | Nonfarm Productivity Q1 P | -7.50% | -5.10% | 6.60% | |

| 12:30 | USD | Unit Labor Costs Q1 P | 11.60% | 7.40% | 0.90% | |

| 14:30 | USD | Natural Gas Storage | 69B | 40B |