European majors are the stronger ones for today, with help from better than expected investor confidence data. Sterling is leading the way, followed by Swiss Franc and Euro. While risk sentiment appears to be mildly positive, there is no clear buying in commodity currencies. Instead, they are the softer ones overall. Dollar and Yen are mixed for now.

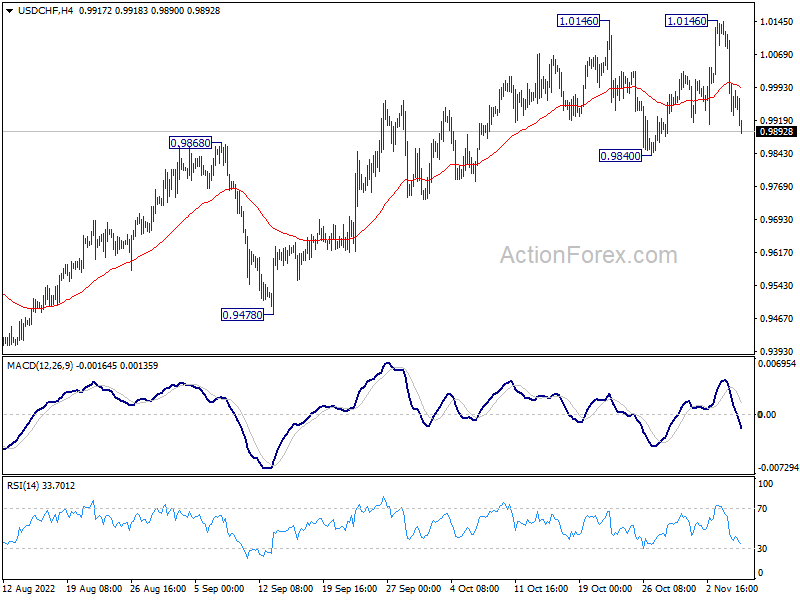

Technically, as European majors are gaining against Dollar, focus is back to respective pair. In particular, firm break of 0.9840 support in USD/CHF will complete a double top pattern, which is rather near term bearish. That would also complete with decisive break of 55 day EMA, and open up deeper fall to 0.9478 support.

In Europe, at the time of writing, FTSE is down -0.23%. DAX is up 0.80%. CAC is up 0.11%. Germany 10-year yield is down -0.0336 at 2.268. Earlier in Asia, Nikkei rose 1.21%. Hong Kong HSI rose 2.69%. China Shanghai SSE rose 0.23%. Singapore Strait times rose 0.36%. Japan 10-year JGB yield rose 0.0015 to 0.258.

Eurozone Sentix investor confidence rose to -30.9, concerns of catastrophic gas shortage fading

Eurozone Sentix Investor Confidence rose from -38.3 to -30.9 in November, above expectation of -35. Current situation index rose from -35.5 to -29.5. Expectations index rose from -41.0 to -32.3, highest since June this year.

Sentix said: “At the beginning of November, the sentix economic indices in Euroland surprise on the positive side. The overall index rises by 7.4 points to -30.9, which is still not a trend reversal signal. But the rise in situation and expectation values shows how sensitively investors react in their economic expectations to signals from the energy market.

“For this is the cause of the hopeful changes. October showed higher temperatures than usual and this means that gas storage facilities in Germany, for example, are full to the brim, more than expected for November. Spot market gas prices collapsed in response. Concerns about a catastrophic gas shortage are fading.”

ECB Villeroy: Hiking pace more flexible, possibly slower beyond neutral rate

ECB Governing Council member Francois Villeroy de Galhau said in an interview, “as long as underlying inflation has not clearly peaked, we shouldn’t stop on rates.”

“It’s too early to tell where the end point in interest rates, or the so-called terminal rate, could be,” Villeroy said. “That said we are not far from the neutral rate, beyond which our hiking pace could be more flexible and possibly slower.”

“We can raise interest rates without provoking significant unemployment,” Villeroy said. “To determine the level of growth next year, energy is more important than monetary policy. Our aim is not to provoke a recession but to tame inflation.”

China exports dropped -0.3% yoy in Oct, imports down -0.7% yoy

In USD term, China’s exports dropped -0.3% yoy to USD 298.37B in October, well below expectation of 4.3% yoy. That’s the worst performance since May 2020.

Imports dropped -0.7% yoy to USD 213.22B, below expectation of 0.1% yoy. That’s the the worst since August 2020.

The simultaneous contraction in both exports and imports was the first since May 2020.

Trade surplus widened slightly from USD 84.74B to USD 85.15B, short of expectation of USD 95.95.

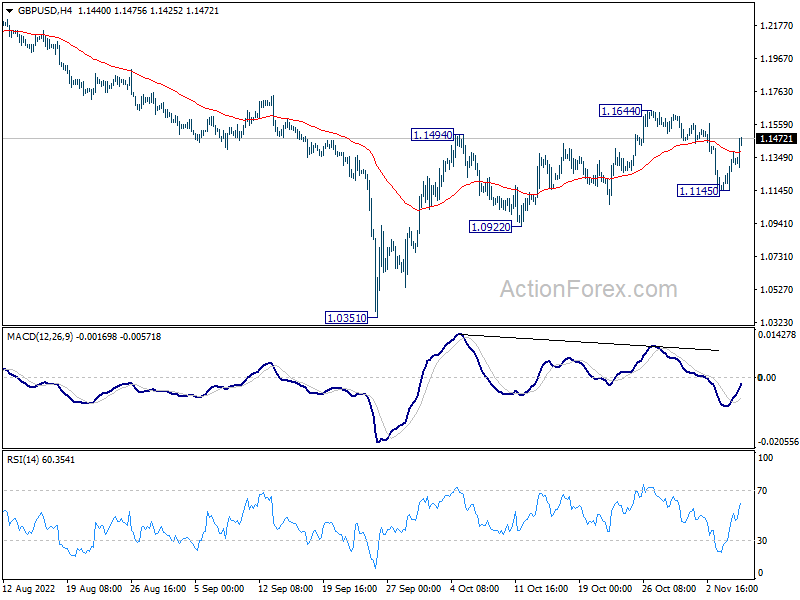

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1223; (P) 1.1302; (R1) 1.1455; More…

GBP/USD’s rebound from 1.1145 extends higher today but stays well below 1.1644 resistance. Intraday bias remains neutral first. On the upside, break of 1.1644 will resume the whole rise from 1.0351 and target 1.1759/2292 resistance zone. On the downside, break of 1.1145 will reaffirm the case that corrective rise from 1.0351 has completed at 1.1644. Deeper fall would then be seen back to 1.0922 support and below.

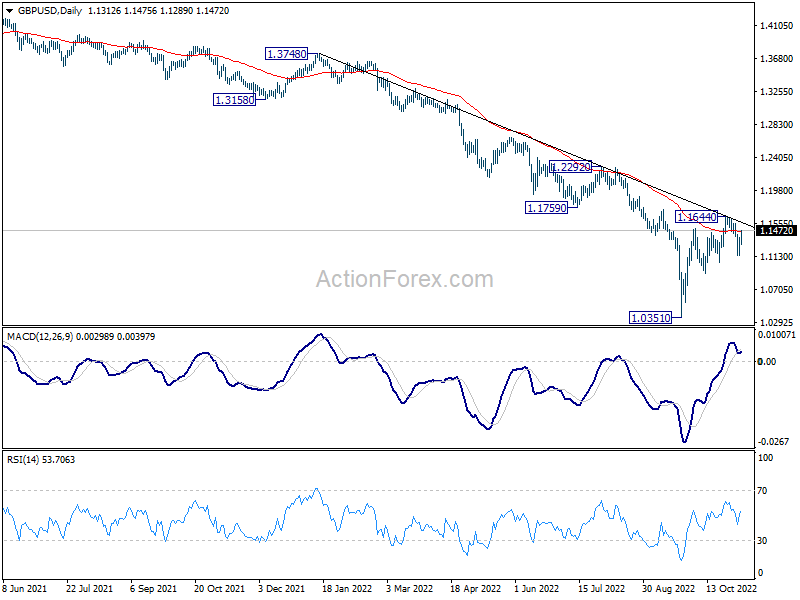

In the bigger picture, fall from 1.4248 (2018 high) is part of the long term down trend from 2.1161 (2007 high). Outlook will stay bearish as long as 1.1759 support turned resistance holds. Parity would be the next target on resumption. Nevertheless, firm break of 1.1759 will confirm medium term bottoming, and open up stronger rise back to 55 week EMA (now at 1.2357).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 02:00 | CNY | Trade Balance (USD) Oct | 85.2B | 96.0B | 84.7B | |

| 02:00 | CNY | Trade Balance (CNY) Oct | 587B | 702B | 574B | |

| 06:45 | CHF | Unemployment Rate Oct | 2.10% | 2.10% | 2.10% | |

| 07:00 | EUR | Germany Industrial Production M/M Sep | 0.60% | -0.20% | -0.80% | |

| 08:00 | CHF | Foreign Currency Reserves (CHF) Oct | 817B | 807B | 806B | |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Nov | -30.9 | -35 | -38.3 |