Trading in the Asian markets is relatively subdued again. Asian stocks are mixed even though DOW and S&P 500 rose to new record highs overnight. Dollar continues to fail to find a committed direction. While the greenback remains firm against Euro, Swiss Franc and Yen, it clearly lacks upside momentum against commodity currencies. With a light calendar today, the markets could need to wait for next week to come back to life.

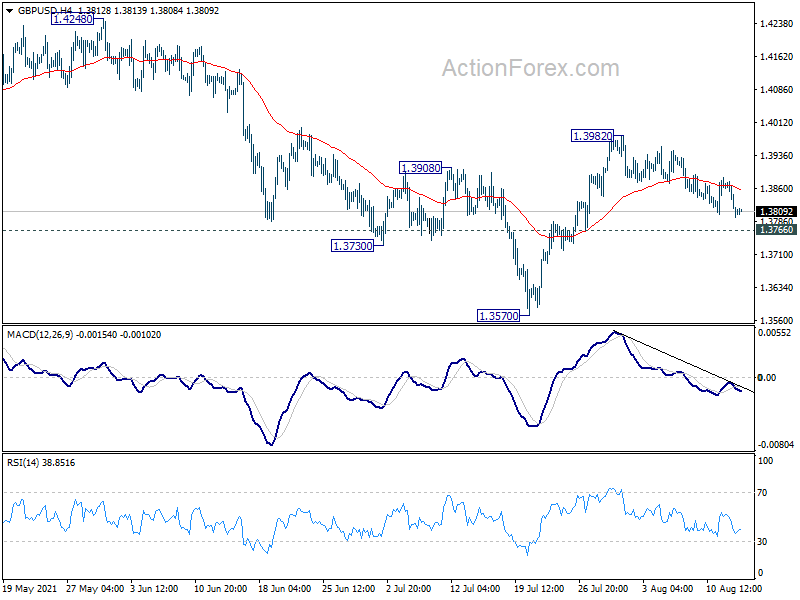

Technically, one development to note is that Sterling is apparently turning weaker against both Euro and Yen. There is prospect of more weakness in the Pound in these two crosses. That, if happens, could trigger deep pull back in GBP/USD through 1.3766 minor support, which in turn feeds back into EUR/GBP and GBP/JPY.

In Asia, at the time of writing, Nikkei is up 0.05%. Hong Kong HSI is down -0.99%. China Shanghai SSE is down -0.37%. Singapore Strait Times is down -0.66%. Japan 10-year JGB Yield is down 0.0006 at 0.025. Overnight, DOW rose 0.04%. S&P 500 rose 0.30%. NASDAQ rose 0.35%. 10-year yield rose 0.028 to 1.367.

New Zealand BusinessNZ manufacturing rose to 62.6, second highest on record

New Zealand BusinessNZ Performance of Manufacturing Index rose from 60.9 to 62.6 in July. That’s the second highest reading after March’s 63.6. Looking at some details, production rose from 64.4 to 66.0.. Employment rose from 56.7 to 58.3, a new record. New orders rose from 63.6 to 65.0. Finished stocks dropped from 57.4 to 56.9. Deliveries rose from 55.2 to 57.9.

However, the position of negative comments (51.4%) still remained higher than positive ones (48.6%). Increased domestic and overseas orders was the common factor for positive comments. In contrast, tight labor market, supply chain issues and raw material costs were the negatives.

BNZ Senior Economist, Craig Ebert stated that “while New Zealand’s PMI is doing exceptionally well, we are also conscious of the headwinds happening for global manufacturing. This is on account of the resurgence of COVID19 in its delta strain.”

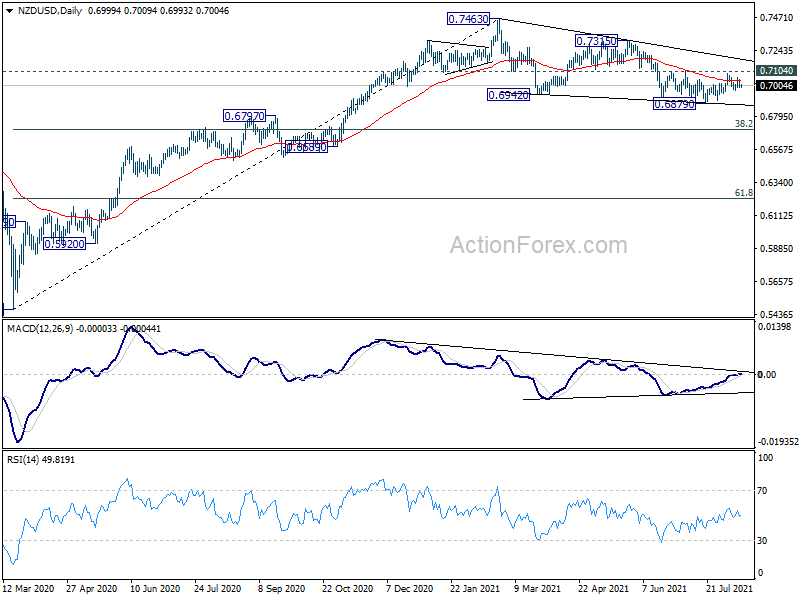

NZD/USD stuck in range, with mild bearish bias

New Zealand Dollar is one of the better performers this week, together with Australian and Canadian. Nevertheless, it’s just stuck in range against Dollar for now. NZD/USD is extending the range pattern from 0.6879. The failure to break through 55 day EMA firmly is keeping near term outlook bearish.

Overall, price actions from 0.7463 are seen as correcting the whole up trend from 0.5467. Downside momentum is diminishing as seen in daily MACD. Hence, in case of another fall, strong support would likely be seen from 38.2% retracement of 0.5467 to 0.7463 at 0.6701 to contain downside. On the upside, break of 0.7104 resistance will suggest that the correction has completed and bring stronger rebound back to 0.7315/7463 resistance zone.

Looking ahead

Swiss PPI and Eurozone trade balance will be released in European session. US will release import price and U of Michigan consumer sentiment.

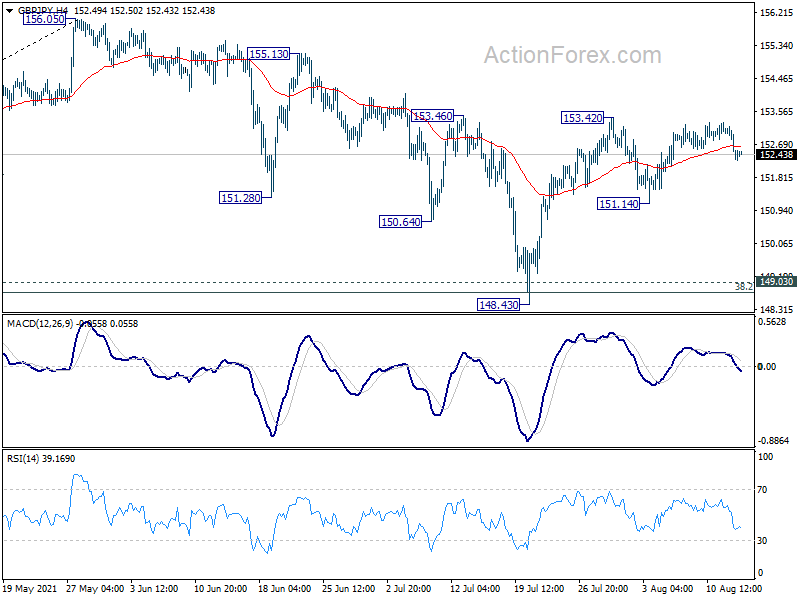

GBP/JPY Daily Outlook

Daily Pivots: (S1) 152.12; (P) 152.67; (R1) 152.99; More…

GBP/JPY drops slightly after failing to break through 153.42 resistance. But it stays in range of 151.14/153.42 and intraday bias remains neutral first. On the upside, break of 153.42/46 resistance will reaffirm the case that correction from 156.05 has completed at 148.43. Intraday bias will be back on the upside for retesting 156.05. On the downside, though, below 151.14 will bring deeper fall back to retest 148.43 instead.

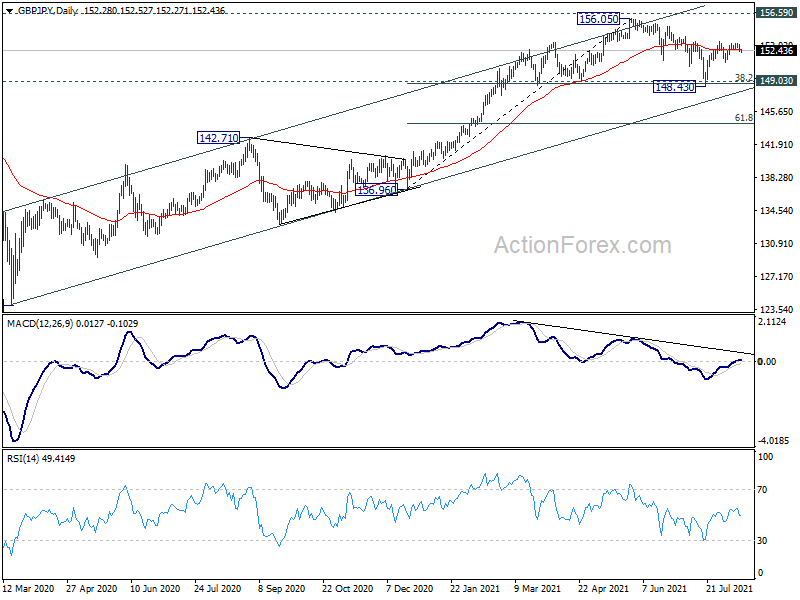

In the bigger picture, rise from 123.94 is seen as the third leg of the pattern from 122.75 (2016 low). Focus remains on 156.59 resistance (2018 high). Sustained break there should confirm long term bullish trend reversal. Next target is 61.8% retracement of 195.86 (2015 high) to 122.75 at 167.93. On the downside, sustained break of 149.03 support, however, will argue that rise from 123.94 has completed. Further break of 142.71 would open up the bearish case for retesting 122.75 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI Jul | 62.8 | 60.7 | 60.9 | |

| 6:30 | CHF | Producer and Import Prices M/M Jul | 0.30% | 0.30% | ||

| 6:30 | CHF | Producer and Import Prices Y/Y Jul | 2.80% | 2.90% | ||

| 9:00 | EUR | Eurozone Trade Balance (EUR) Jun | 9.3B | 9.4B | ||

| 12:30 | USD | Import Price Index M/M Jul | 0.60% | 1.00% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Aug P | 81.3 | 81.2 |