Swiss Franc is trading broadly lower today while Yen and Aussie are also turning weaker. The theme for now is interesting will stay higher for longer due to resilience in major economies. Monetary policy in Japan and Swiss will be lagging behind. Dollar is staying generally firm and looks set to extend recent rally. Rising US treasury yields are giving the greenback a hand. But the main driver will continue to be overall risk sentiment.

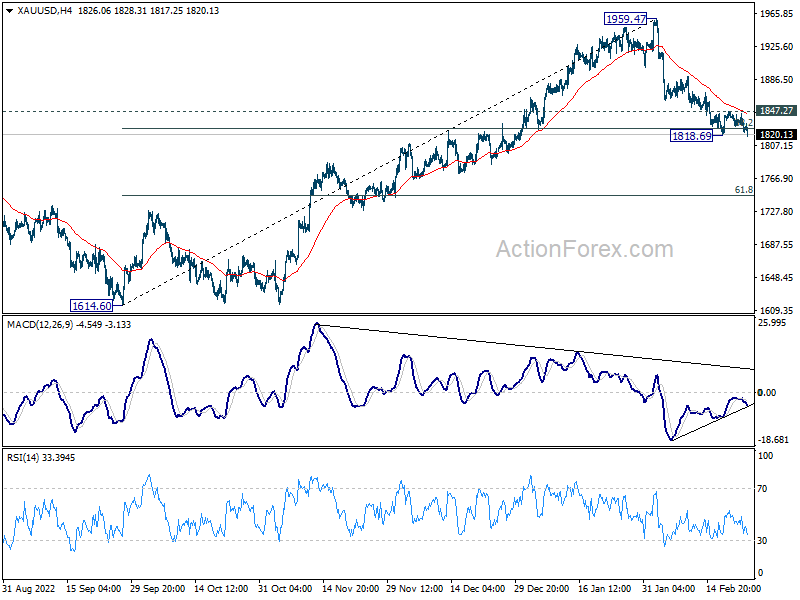

Technically, Gold’s fall from 1959.47 is trying to resume and it’s now pressing 1818.69 support. Firm break there, and sustained trading below 38.2% retracement of 1614.60 to 1959.47 at 1827.72 will pave the way to 1746.34. On the other hand, rebound from current level, followed by break of 1847.27 minor resistance will confirm short term bottoming and bring stronger rebound.

In Europe, at the time of writing, FTSE is down -0.21%. DAX is up 0.46%. CAC is up 0.25%. Germany 10-year yield is up 0.027 at 2.551. Earlier in Asia, Hong Kong HSI dropped -0.35%. China Shanghai SSE dropped -0.11%. Singapore Strait Times dropped -1.06%. Japan was on holiday.

US initial jobless claims dropped to 192k, better than expectations

US initial jobless claims dropped -3k to 192k in the week ending February 18, better than expectation of 200k. Four-week moving average of initial claims rose 1.5k to 191k.

Continuing claims dropped -37k to 1654k in the week ending February 11. Four-week moving average of continuing claims dropped -3k to 1669k.

Also released, Q4 GDP growth was revised down to 2.7% annualized.

BoE Mann: More tightening is needed, a pivot is not imminent

BoE MPC member Catherine Mann said in a speech that while monetary policy taken has been historically aggressive, it’s perhaps “insufficiently so relative to the multiple shocks, the behaviours pushing up inflation, and the initial accommodative starting point”.

“The stage was set for a transmission of monetary policy to financial markets that has been quick, but also has been partially absorbed,” she said. “And… are already incorporating the expected future inflection in monetary stance.

“All this adds up to financial conditions that are now looser than what likely will be needed to moderate the embedding of on-going inflation into the wage- and price-setting paths.”

“This constellation could yield extended persistence of inflation into this year and the next. The resulting long period of time above the 2% target could increase the degree of backward-lookingness, or catch-up behaviour, in the system.”

“Given that the risk of increasingly persistent inflation rises disproportionately with the share of backward-lookingness, I believe that more tightening is needed, and caution that a pivot is not imminent. In my view, a preponderance of turning points (Mann, 2023) is not yet in the data.”

Eurozone CPI finalized at 8.6% yoy in Jan, core CPI at 5.3% yoy

Eurozone PMI was finalized at 8.6% yoy in January, down from 9.2% yoy in December. CPI core (all items ex-food, alcohol and tobacco) was finalized at 5.3% yoy, up from prior month’s 5.2% yoy.

In January, the highest contribution to the annual Eurozone inflation rate came from food, alcohol & tobacco (+2.94%), followed by energy (+2.17%), services (+1.80%) and non-energy industrial goods (+1.73%).

RBNZ Orr: Cyclone rebuilding could add 1% to GDP over coming years

RBNZ Governor Adrian Orr told Bloomberg TV that rebuilding after the damage by cyclone Gabrielle is expected to boost activity and raise price pressure. There is a risk that OCR might be required to stay higher for longer as a result.

“We’re looking at about a 1% addition to GDP over coming years,” Orr said. “That is well manageable within the current monetary settings. But if inflation expectations continue, if core inflation is more persistent, then tighter for longer is certainly an outcome.”

On the other hand, some of the global downside risks are “actually assisting on the inflation battle,” Orr noted. “Economies are evolving broadly as anticipated, excluding these ongoing shocks. So I’m very confident that low and stable inflation will return.”

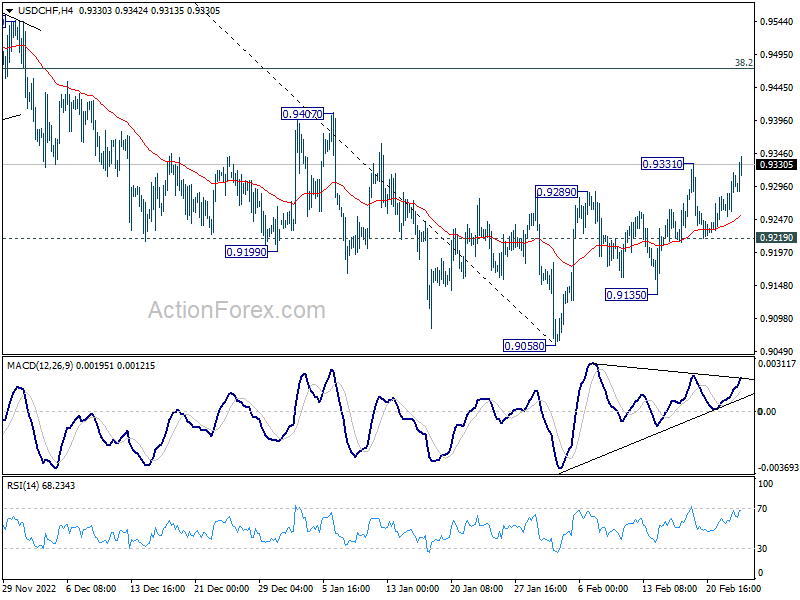

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9271; (P) 0.9295; (R1) 0.9337; More…

USD/CHF’s rise from 0.9058 is resuming by taking out 0.9931 resistance. Intraday bias is back on the upside for 38.2% retracement of 1.0146 to 0.9058 at 0.9474. For now, break of 0.9219 support is needed to indicate completion of the rebound. Otherwise, further rally will remain in favor in case of retreat.

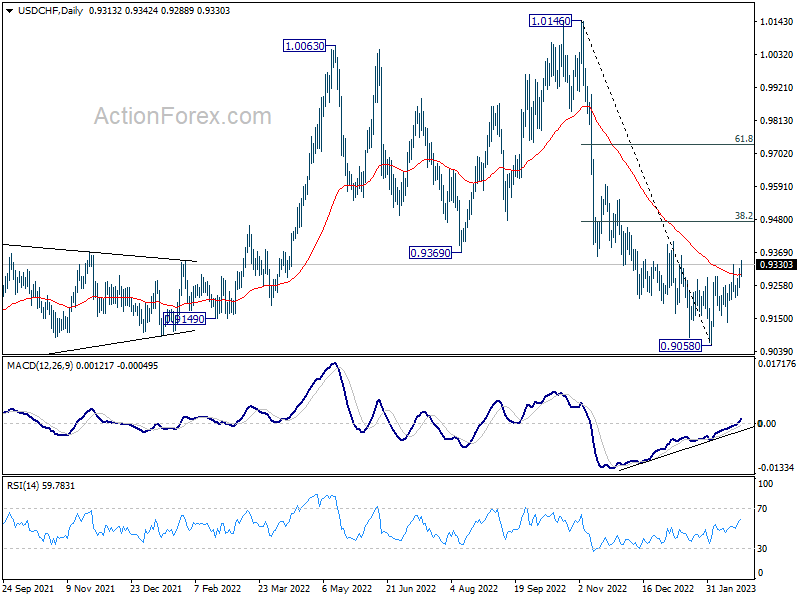

In the bigger picture, decline from 1.0146 is seen as part of a long term sideway pattern. As long as 38.2% retracement of 1.0146 to 0.9058 at 0.9474 holds, another fall is in favor through 0.9058. However, sustained trading above 0.9474 will indicate that the medium term trend has reversed, and open up further rally to 1.0146 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Private Capital Expenditure Q4 | 2.20% | 1.40% | -0.60% | |

| 10:00 | EUR | Eurozone CPI Y/Y Jan F | 8.60% | 8.50% | 8.50% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Jan F | 5.30% | 5.20% | 5.20% | |

| 13:30 | USD | Initial Jobless Claims (Feb 17) | 192K | 200K | 194K | 195K |

| 13:30 | USD | GDP Annualized Q4 P | 2.70% | 2.90% | 2.90% | |

| 13:30 | USD | GDP Price Index Q4 P | 3.90% | 3.50% | 3.50% | |

| 15:30 | USD | Natural Gas Storage | -60B | -100B | ||

| 16:00 | USD | Crude Oil Inventories | 2.9M | 16.3M |