Swiss Franc is currently the strongest performer for the day, showing a notable gain the Euro. Japanese Yen and Australian Dollar follow closely, indicating that the market moves are not predominantly driven by risk aversion. In contrast, New Zealand Dollar is the weakest, as lower-than-expected inflation data increases hopes that RBNZ is nearing a pause in its rate hikes. The Canadian Dollar is the second-worst currency for the day, as it trails falling oil prices. Dollar is on the softer side, as it follows declining Treasury yields. Euro is mixed, seemingly unaffected by comments from ECB officials and the release of March meeting minutes.

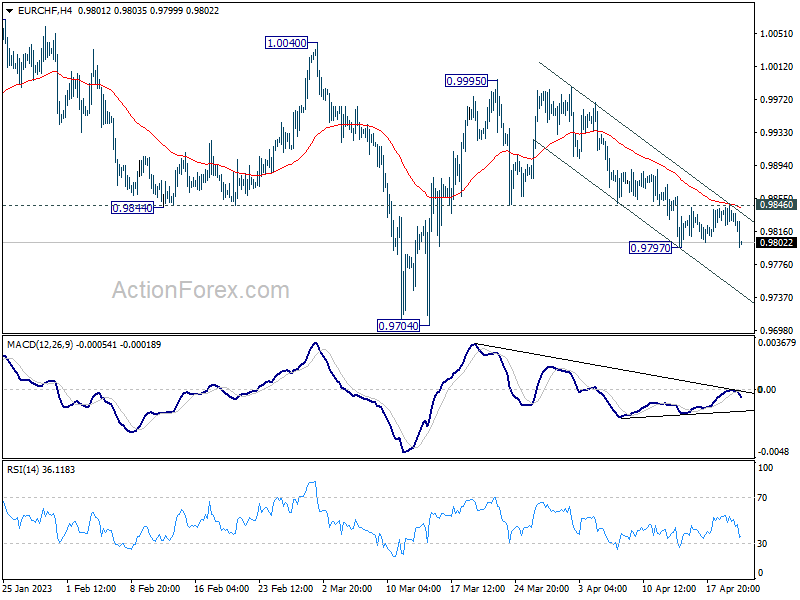

From a technical perspective, EUR/CHF appears ready to resume its decline from 0.9995, passing the temporary low of 0.9797. This drop is considered part of the corrective pattern from the January high of 1.0095. Deeper fall to 0.9704 support and below is expected. If there is a firm break below 0.9797, downside acceleration could exert pressure on Euro in other pairs, limiting its rally momentum.

In Europe, at the time of writing, FTSE is down -0.16%. DAX is down -0.86%. CAC is down -0.37%. Germany 10-year yield is down -0.0412 at 2.475. Earlier in Asia, Nikkei rose 0.18%. Hong Kong HSI rose 0.14%. China Shanghai SSE dropped -0.09%. Singapore Strait Times dropped -0.32%. Japan 10-year JGB yield is down -0.0078 at 0.470.

US initial jobless claims rose to 245k, above expectations

US initial jobless claims rose 5k to 245k in the week ending April 15, above expectation of 238k. Four-week moving average of initial claims dropped -500 to 249.75k.

Continuing claims rose 61k to 1865k in the week ending April 8, highest since November 27, 2021. Four-week moving average of continuing claims rose 15k to 1827k, highest since December 18, 2021.

ECB minutes show majority support for 50bps hike despite market uncertainty

In ECB’s minutes of its March 15-16 meeting, it was revealed that “a very large majority” of members agreed with Chief Economist Philip Lane’s proposal to raise key interest rates by 50 basis points. This decision was made “in line with the intention the Governing Council had communicated at its last monetary policy meeting.”

The minutes noted that “following the announced intended interest rate path was seen as important to instil confidence and avoid creating further uncertainty in financial markets.” However, “some members would have preferred not to increase the key rates until the financial market tensions had subsided and to conduct a comprehensive re-evaluation of the stance at the Governing Council’s next monetary policy meeting, in May.”

Looking ahead, members concurred on the importance of a data-dependent approach for future policy rate decisions amid the “elevated level of uncertainty.” In this context, the minutes stated that “it was underlined that if the inflation outlook embedded in the March ECB staff projections were confirmed, the Governing Council would have further ground to cover in adjusting the monetary policy stance to ensure a timely return of inflation to target.”

ECB’s Knot: Sufficiently restrictive is clearly not where we are today

ECB Governing Council member Klaas Knot has expressed concerns about the current high inflation rate, suggesting that the current mildly restrictive monetary policy may not be enough to counter it.

Knot stated, “We are now in what I would call mildly restrictive territory with policy rates but inflation is not mild. Inflation is still much too high.”

Knot added that the underlying inflation rate, which has been creeping up towards six per cent, needs a sufficiently restrictive stance to be countered. “Where is sufficiently restrictive, I don’t know but clearly not where we are today,” he said.

The ECB policymaker also noted that it is too early to discuss a pause in tightening measures. “For a pause, I would really need to see a convincing reversal in underlying inflation dynamics,” Knot explained.

Eurozone posted first monthly trade surplus since Sep 2021

Eurozone goods exports to the rest of the world rose 7.6% yoy in February to EUR 232.7B. Goods imports rose 1.1% yoy ton EUR 228.1B. Trade surplus came in at EUR 4.6B, the first surplus since September 2021. Intra-Eurozone trade rose 8.0% yoy to EUR 224.4B.

In seasonally adjusted term, exports rose 1.2% mom to EUR 243.9B. Imports dropped -3.4% mom to EUR 252.6B. Trade deficit narrowed to EUR -0.1B, versus expectation of EUR -8.5B. Intra-Eurozone trade rose from February’s EUR 230.7B to EUR 232.3B.

New Zealand CPI slows in to 6.7% Q1, RBNZ may conclude rate hike cycle soon

In Q1, New Zealand CPI growth slowed down from prior quarter’s 7.2% yoy, registering a 6.7% yoy increase, falling short of the expected 7.0% yoy. The largest contributor to the annual inflation rate was the food sector, followed by housing and household utilities.

On a quarterly basis, CPI rose by 1.2% qoq in Q1, below the anticipated 1.5% qoq increase, marking the lowest result in two years. Vegetables and fruit were the primary drivers of food prices, rising by 8.6% and 11%, respectively.

These figures came in lower than RBNZ’s forecast of a 1.8% qoq and 7.3% yoy inflation. Despite the slowdown in inflation, another 25bps rate hike is still anticipated in May due to the persistently high inflation levels. However, it appears increasingly likely that the upcoming rate hike will be the last in the current cycle.

Australia NAB quarter business conditions resilient, but confidence clearly negative

Australia NAB Quarterly Business Confidence dropped from -1 to -4 in Q1. Current Business Conditions fell from 20 to 16. Business Conditions for the next three months decreased from 22 to 19. But Business Conditions for the next 12 months rose from 18 to 20.

“Consistent with our monthly business survey, today’s release confirms business conditions remained resilient through the first quarter of 2023 at levels well above average,” said NAB Chief Economist Alan Oster. “This strength remains broad based and leading indicators are also holding up, although business confidence is now clearly negative.”

Japan sees 25th consecutive month of export growth, record trade deficit in fiscal 2022

In March, Japan’s exports rose 4.3% yoy to JPY 8824B, above expectation of 2.6% yoy. This marks the 25th consecutive month of growth, primarily driven by auto shipments to the United States.

By region, exports to the US increased by 9.4% yoy in March, slowing down from prior month’s 14.9% yoy growth. On the other hand, exports to China, Japan’s largest trading partner, declined by -7.7% yoy marking the fourth consecutive month of decline.

Imports rose 7.3% yoy to JPY 9579B, below expectation of 11.4% yoy. Consequently, Japan registered a trade deficit of JPY -755 billion.

In fiscal 2022 ended March, Japan recorded a record trade deficit of JPY -21.73T, surpassing prior record of JPY -13.76T registered in fiscal 2013. Imports rose 32.2% to JPY 120.95T while exports rose 15.5% to JPY 99.23T.

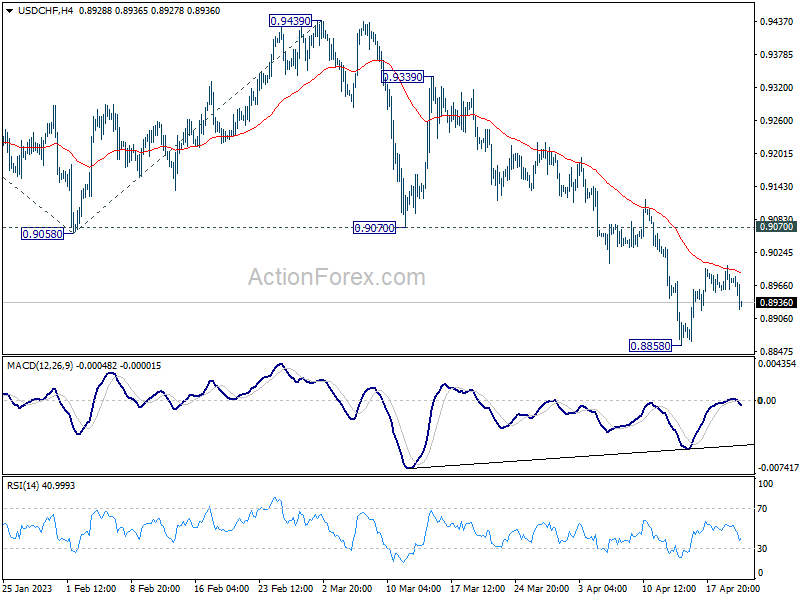

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8955; (P) 0.8979; (R1) 0.9000; More…

USD/CHF dips notably after rejection by 55 4H EMA, but stays well above 0.8858 low. Intraday bias remains neutral for the moment. Another decline cannot be ruled out with 0.9070 support turned resistance intact. On the downside, below 0.8858 will resume the down trend to 61.8% projection of 1.0146 to 0.9058 from 0.9439 at 0.8767, which is close to 0.8756 long term support. Strong support is expected there to bring rebound, at least on first attempt. On the upside, break of 0.9070 support turned resistance will confirm short term bottoming and turn bias back to the upside.

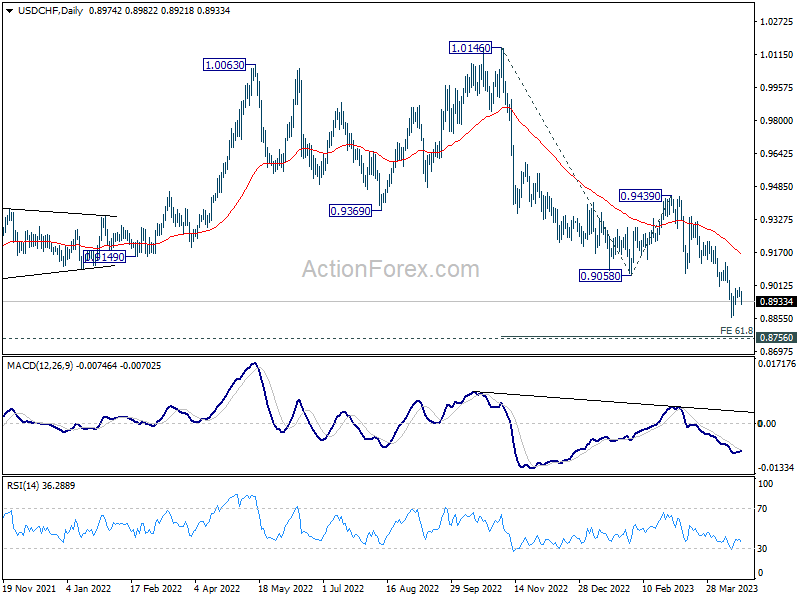

In the bigger picture, fall from 1.1046 (2022 high) is in progress for 0.8756 support (2021 low). But overall, this fall is still seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | CPI Q/Q Q1 | 1.20% | 1.50% | 1.40% | |

| 22:45 | NZD | CPI Y/Y Q1 | 6.70% | 7.00% | 7.20% | |

| 23:50 | JPY | Trade Balance (JPY) Mar | -1.21T | -1.78T | -1.19T | -1.25T |

| 01:30 | AUD | NAB Business Confidence Q1 | -4 | -1 | ||

| 04:30 | JPY | Tertiary Industry Index M/M Feb | 0.70% | 0.40% | 0.90% | 0.70% |

| 06:00 | EUR | Germany PPI M/M Mar | -2.60% | -0.50% | -0.30% | |

| 06:00 | EUR | Germany PPI Y/Y Mar | 7.50% | 9.80% | 15.80% | |

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:30 | USD | Initial Jobless Claims (Apr 14) | 245K | 238K | 239K | 240K |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Apr | -31.3 | -19.1 | -23.2 | |

| 14:00 | USD | Existing Home Sales Mar | 4.50M | 4.58M | ||

| 14:00 | EUR | Eurozone Consumer Confidence Apr P | -18 | -19 | ||

| 14:30 | USD | Natural Gas Storage | 69B | 25B |