Last week, the world appeared to be on the brink of an international banking crisis. The situation might have stabilized with Silicon Valley Bank filing for Chapter 11 bankruptcy, First Republic Bank receiving aid in the form of deposits from major players, and Credit Suisse obtaining a CHF 50B lifeline from SNB. Despite these developments, market reactions suggest investors may be positioning for worse outcomes ahead.

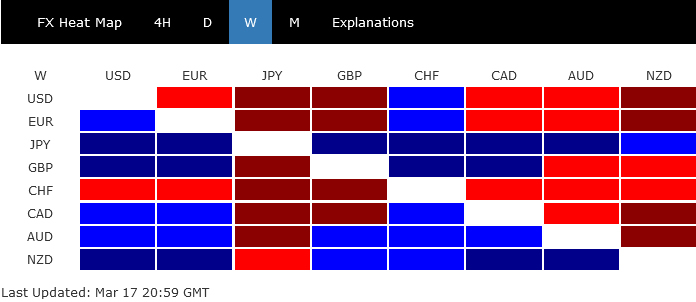

In the currency markets, Yen emerged as the clear winner due to risk aversion and a boost from falling benchmark treasury yields in US and Europe. Swiss Franc, Dollar, and Euro were the weakest performers as the crisis unfolded on two fronts. Australian and New Zealand Dollars showed surprising resilience, but this is likely because they were not at the center of the storm.

Risk-off moves gather steam, suggesting more turbulence ahead

A casual glance at US stock performance might not reveal the full extent of last week’s market upheaval caused by the banking crisis. While the DOW registered some losses, both S&P 500 and NASDAQ closed higher. However, the situation in Europe paints a different picture, with FTSE 100 experiencing its worst week in a year, dropping 5.3%, and DAX losing 4.3%.

In the bond market, the US 2-year yield saw its largest weekly decline in over 35 years, closing at 3.825. 10-year yield dropped to 3.395, while Germany’s 10-year yield fell to its lowest level since early February at 2.110. UK 10-year yield also dipped to an early-February low of 3.287.

Safety-seeking funds didn’t just flow into bonds. Gold surged more than 5.5%, its most significant gain since March 2020, and appears poised to challenge historical highs. Bitcoin, considered by some as a safe haven asset for now, broke through a crucial technical resistance at around 25,000 and reached its highest level in nine months. In contrast, WTI crude oil, not typically considered a safe asset, plunged to a 15-month low.

The strong momentum of moves in FTSE, DAX, and Gold suggests that market turbulence is far from over. Three central banks are set to meet in the coming days, and all are expected to continue tightening. Most market participants anticipate 25bps hikes from Fed and BoE, with a 50bps hike expected from SNB. However, the final outcomes will heavily depend on developments leading up to the meetings. Furthermore, the results themselves are likely to contribute to market volatility. So, brace for potential turbulence ahead.

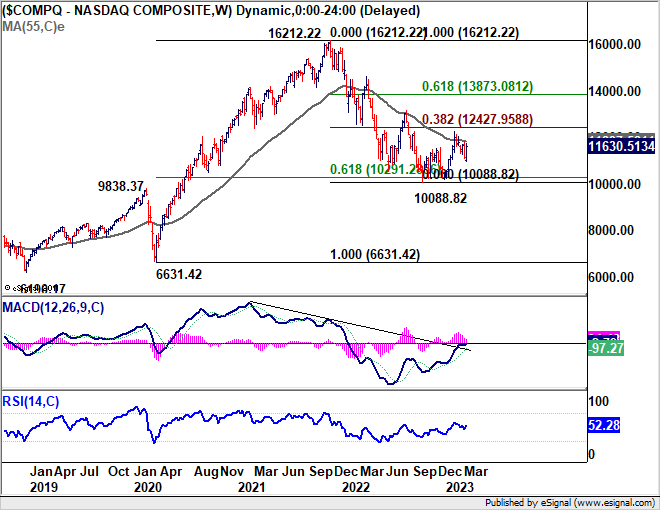

Rare display of optimism in NASDAQ

In a rare display of optimism last week, the NASDAQ experienced a robust rebound. This development indicates that the corrective pullback from 12269.55 may have completed at 10982.80. In the coming days, the immediate focus will shift to 11827.92 resistance level. A decisive break above this level would likely resume the overall rebound from 10,088.82, pushing through 12269.55 towards 38.2% retracement of 16212.22 to 10088.82 at 12427.95. However, the trajectory of the NASDAQ will also hinge on developments in other markets.

FTSE faces deep trouble, DAX vulnerable as well

FTSE’s sharp decline and close below its 55 week EMA (now at 7446.94) suggest that 8047.06 record high may represent at least a medium-term peak. More significantly, the uptrend from the 2020 low of 4898.79 could have reached completion as a five-wave impulse. As FTSE enters a correction phase, near-term outlook remains bearish, as long as 55 day EMA (now at 7734.20) holds. Deeper fall could be seen to 38.2% retracement of 4898.79 to 8047.06 at 6844.42 before bottoming.

Though the outlook for DAX is less negative than that of FTSE, it remains concerning. The break below its 55 day EMA (now at 15066.64) implies that a medium-term top has formed at 15706.37, accompanied by bearish divergence in daily MACD. In the near term, DAX is expected to decline further to 38.2% retracement of 11862.84 to 15706.37 at 14238.14. Sustained break at this level, and below the 55 week EMA (now at 14314.46), would indicate the start of the third leg of the corrective pattern from 16290.19 (2021 high). Such a development would pave the way for a deeper fall toward the 2022 low of 11862.84 (2022 low).

US 10-year yield to extend correction through 3.334

Turning over to the bond markets, US 10-year yield extended the decline from 4.091 to close at 3.395. Although the fall may have slowed slightly ahead of 3.334 support level, risk remains heavily skewed to the downside as long as the 55 day EMA (now at 3.717) holds. TNX is now in the third leg of its medium-term correction from 4.333.

Significant support could emerge from 61.8% retracement level of 2.525 to 4.333 at 3.215, which is in close proximity to 55 week EMA (now at 3.220). This zone may provide a solid foundation for TNX to bottom out. However, a sustained break through the 3.2 handle would signal even larger troubles on the horizon.

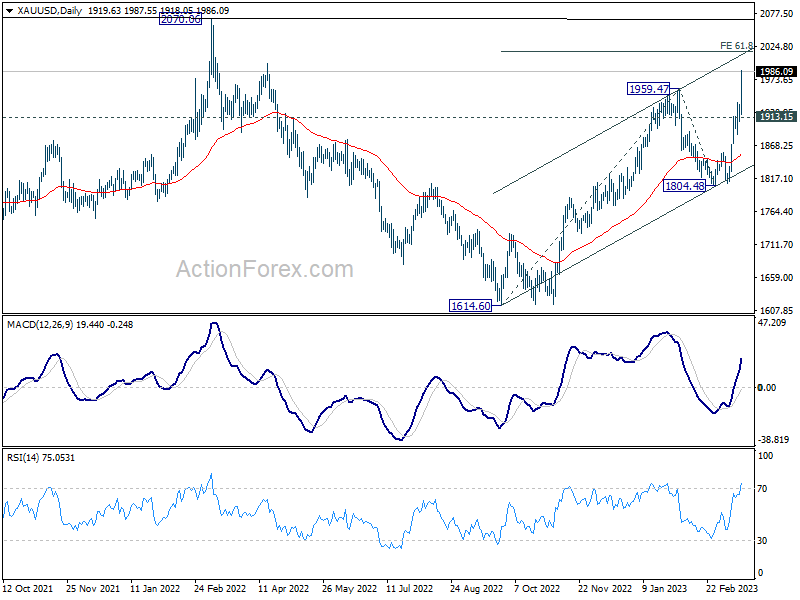

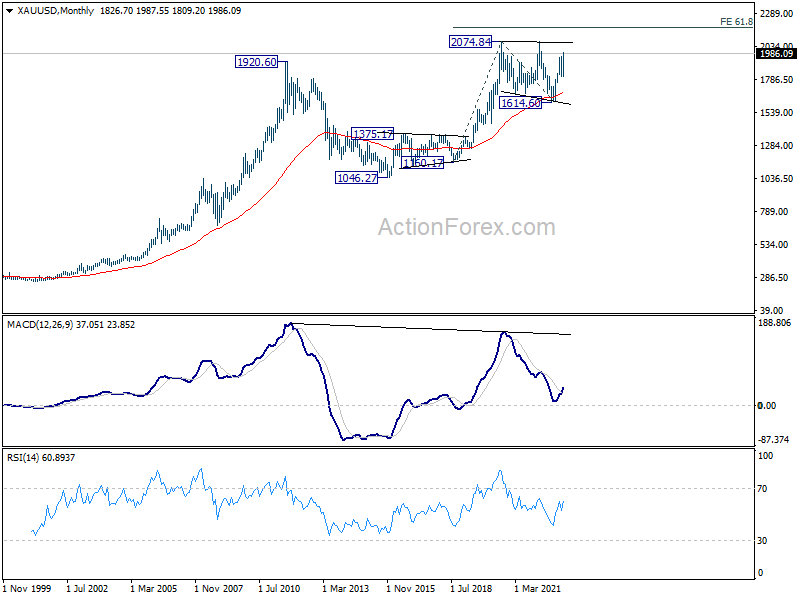

Gold’s resurgence signals potential retest of record highs

Gold’s rise from 1614.60 resumed last week by powering through 1969.47 resistance to close at 1986.09. Near-term outlook will remain bullish as long as the 1913.15 support holds. The next target is the 61.8% projection of 1614.60 to 1959.47 from 1804.48 at 2017.60. A firm break through this level will pave the way for a retest of the 2074.84 record high.

More significantly, the current upside momentum strengthens the argument that long-term consolidation pattern from the 2074.84 (2020 high), with three waves down to 1615.60, has been completed. The long-term uptrend could be set to resume, potentially reaching the 61.8% projection of 1160.17 to 2074.85 from 1614.60 at 2179.86 in Q2.

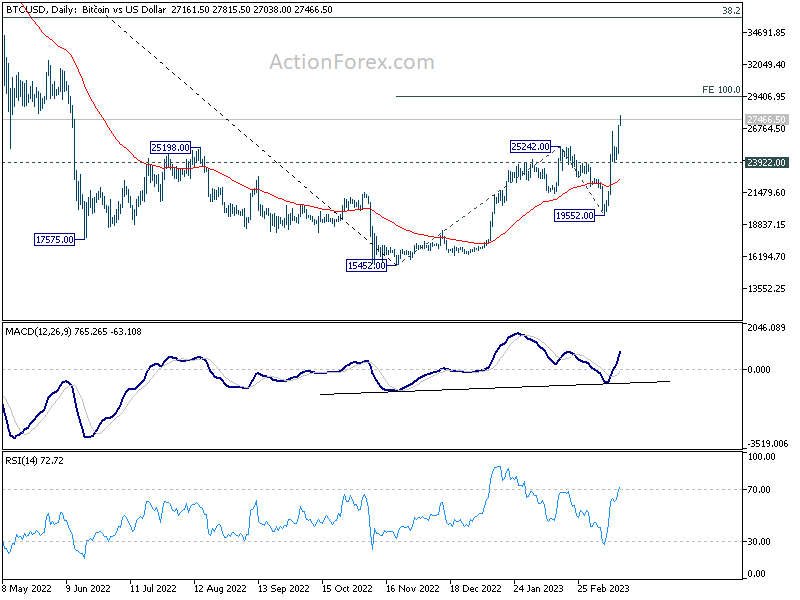

Bitcoin’s rally carries bullish implications amid market uncertainty

The role of Bitcoin as a safe-haven asset or a barometer for the tech sector remains a topic of debate. Nevertheless, last week’s rally and the strong break through 25198/25242 resistance zone, along with 55 week EMA, point to bullish implications. Rise from 15452 appears to be at least a correction to the downtrend from record high of 68986 set in 2021.

Near-term outlook for Bitcoin will remain bullish as long as 23922 support level holds. Next target is 100% projection of 15452 to 25242 from 19552 at 29342. A decisive break through this level would affirm the bullish case mentioned above and set sights on the 38.2% retracement of 68986 to 15452 at 35901.

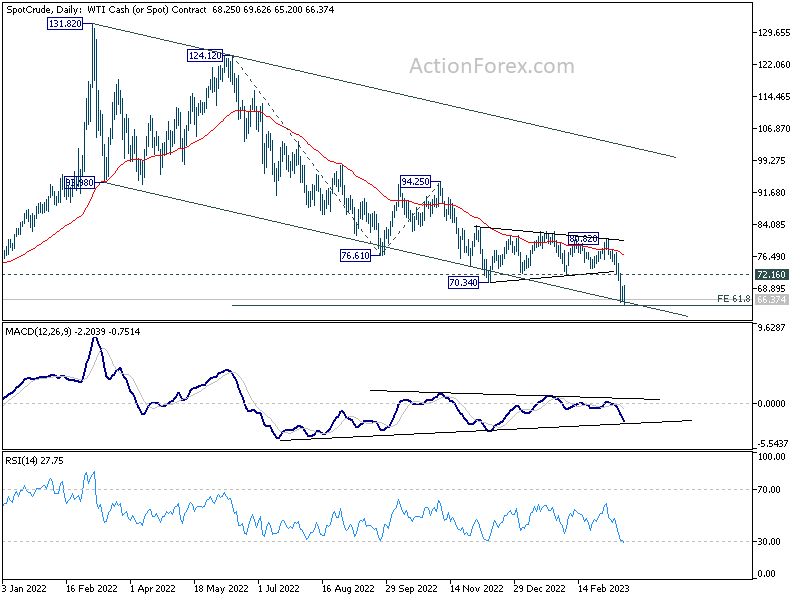

WTI crude oil to search for a bottom after tumbling, could it?

Whether it’s due to recession fears or the banking crisis, WTI crude oil tumbled sharply last week, closing at 66.37 after being briefly above 80 just two weeks ago. Theoretically, this price range is where WTI could find its bottom. It’s close to the 61.8% projection of 124.12 to 76.61 from 94.25 at 64.88, and nearing the long-term channel support at around 65.54. A break above 72.16 support-turned-resistance level would be the first sign of stabilization.

However, a firm break below 64.88 could trigger an even steeper decline with downside acceleration. In that case, 100% projection at 46.74 could be easily within reach.

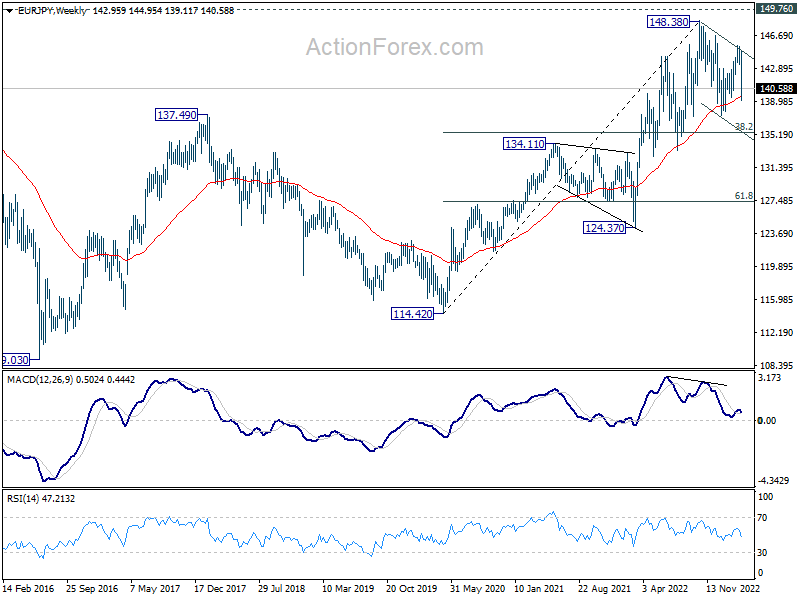

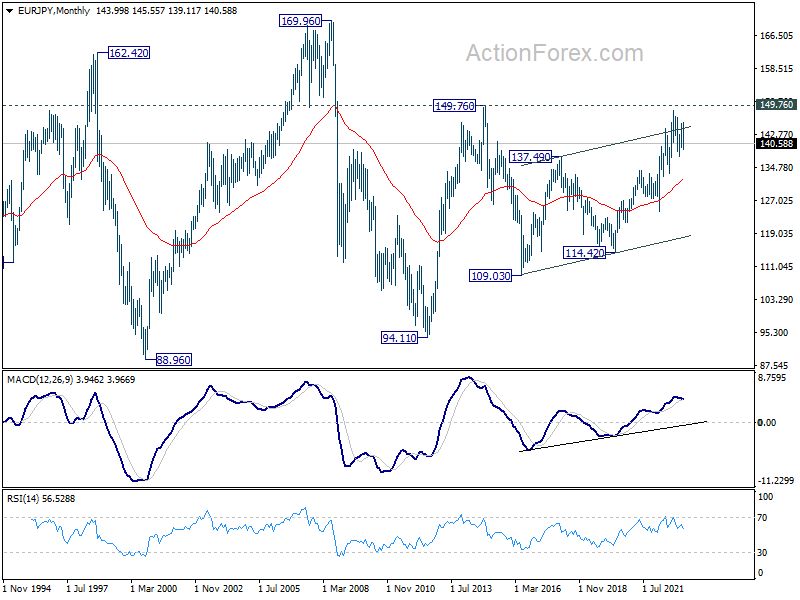

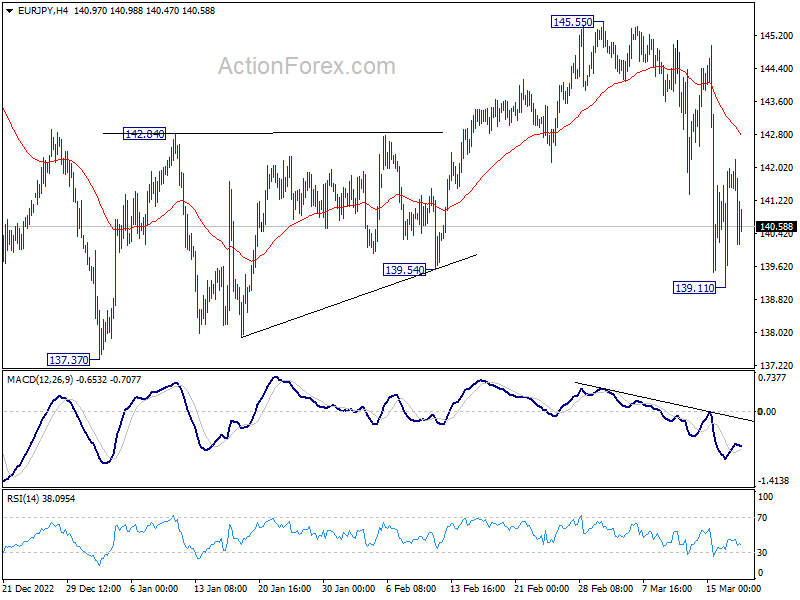

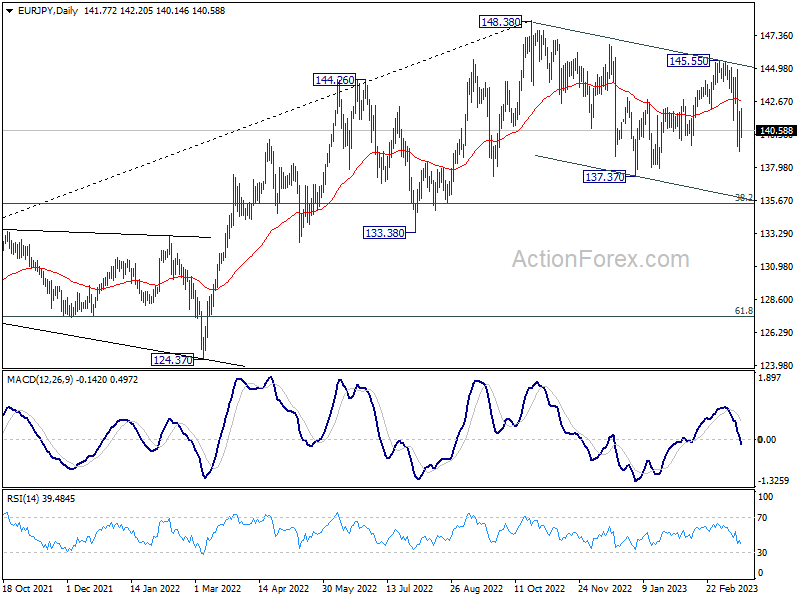

EUR/JPY Weekly Outlook

EUR/JPY fell to as low as 139.11 last week before forming a temporary low there and recovered. Current development suggests that fall from 145.55 is the third leg of the whole corrective decline from 148.38. Risk stays on the downside as long as 4 hour 55 EMA (now at 142.85) holds. Below 139.11 will target 137.37 low, and then 135.40 fibonacci level.

In the bigger picture, as long as 55 week EMA (now at 139.54) holds, larger up trend from 114.42 (2020 low) is still in progress for 149.76 long term resistance. However, firm break of 55 week EMA will bring deeper fall to 38.2% retracement of 114.42 to 148.38 at 135.40. Sustained break there will raise the chance of trend reversal, and target 61.8% retracement at 127.39.

In the long term picture, outlook will stay bullish as long as 134.11 resistance turned support holds (2021 high). Sustained break of 149.76 (2014 high) will open up further rally, as resumption of the rise from 94.11 (2012 low), towards 169.96 (2008 high).