10 year yields were lower. Most stock indices were higher. Crude oil is up for the 3rd week in a row.

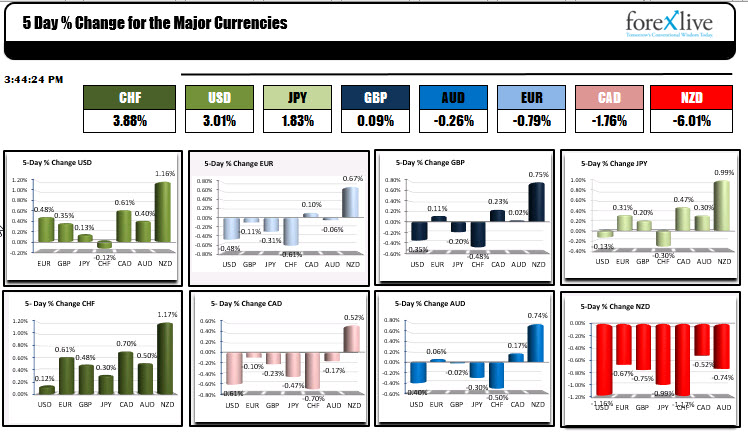

The CHF was the strongest of the major currencies for the week of June 7 to June 11. The NZD was the weakest.

The USD is ending mostly higher with 5-day gains vs all the major currencies with the exception of the CHF where it was down only -0.12%. The greenback rose the most vs the NZD (+1.16%).

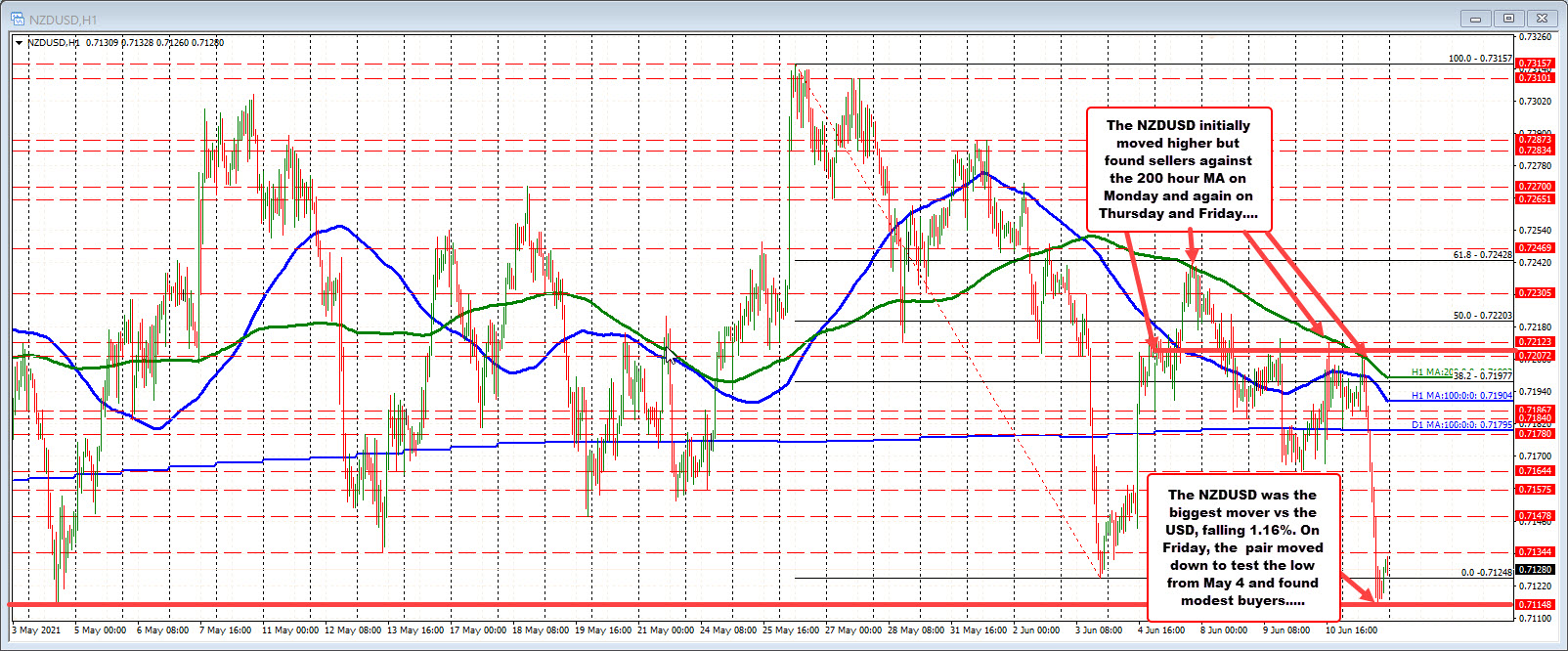

Looking at the NZDUSD the pair initially moved higher on Monday, only to find sellers vs the 200 hour MA (green line). That MA line was tested on Thursday and Friday before sellers pushed the pair down sharply on Friday to test the low going back to May 4. Buyers leaned against that level and modestly rose into the week’s close. That low will be a key barometer in the new trading week.

In other markets for the week,

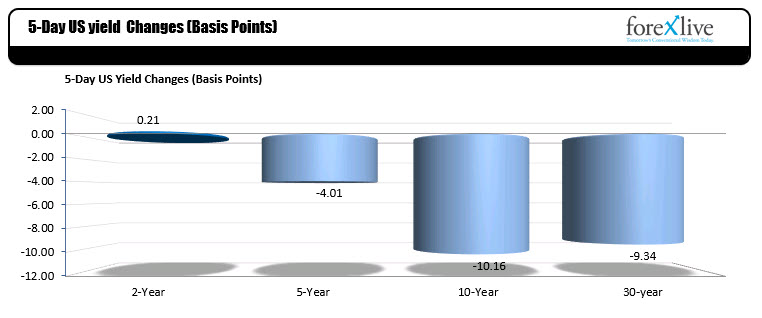

- US treasury yields moved lower after the successful auction of 3, 10 and 30 year issues, and the maneuvering through what was higher CPI numbers for May. The 10 year yield moved below the 1.5% level (the high cycle yield reached 1.774% on March 30), and closed below the 100 day MA at 1.493% for the first time since October 2020. For the week, the 10 year yield fell -10.16 basis points to 1.4518%. The 30 year was down -9.34 basis points to 2.1379%, while the 2 year yield rose by 0.21 basis points to 0.1469%. The traders seem content to follow the Fed’s lead that inflation will be transitory. The FOMC meets this week on Tuesday with the decision at 2 PM on Wednesday and Chair Powell presser on Wednesday at 2:30 PM ET. The market will be focused on any references to tapering from the statement or the Fed chair. Rates are not close to being changed.

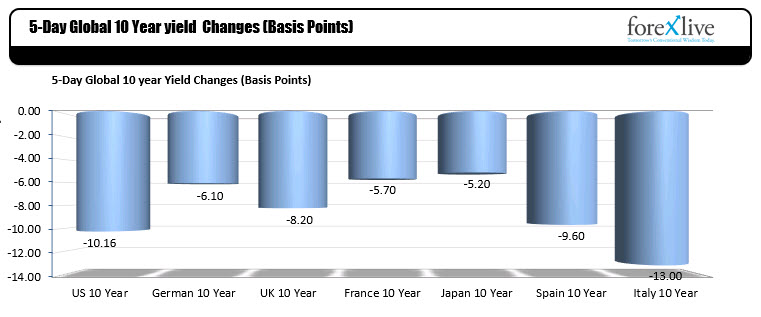

- Looking at other 10 year yields from around the globe, the Italian 10 year yield fell the most (-13 basis points). The German 10 year fell -6.1 basis points while France’s yield fell by -5.7 basis points and is at 0.097% (and getting closer to 0.0% again). In the new trading week, the SNB will keep rates unchanged at -0.75% on Thursday. The focus will be on the language. SNB Jordan continues to view the CHF as “very strong”. The BOJ rate decision will be Friday and they too are expected to keep rates unchanged at -0.1% and the 10 year JGB yield target at 0.0% (with tolerance of +/-25BPS).

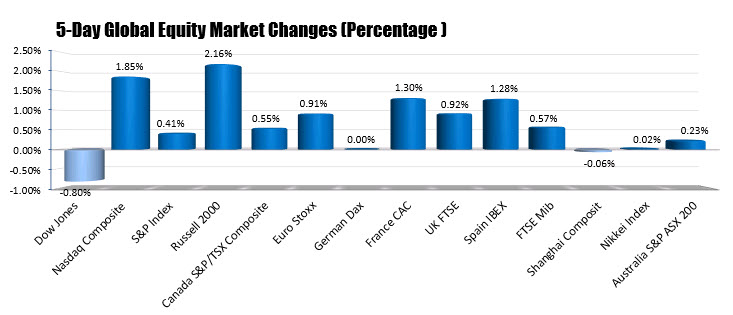

- Most major global stock indices moved higher this week with the exception of the Dow 30 (-0.8%) and the Shanghai Composite index (-0.06%). The biggest gainer was the small cap Russell 2000 index (US) which rose 2.16%. In Europe, the France’s CAC nudged out Spain’s Ibex as the biggest gainer (1.3% vs 1.28%).

This article was originally published by Forexlive.com. Read the original article here.